Last year around this time, I wrote a reflection on our first year of the blog. It’s amazing to think that we’ve already hit the second year milestone already!

In that post, I recapped my favorite posts from our first 132,000 words. Specifically, I discussed the posts that shared the most about our story and our mindset shifts. We learned a lot during our first year of FI and our first year of writing the blog that we wanted to share with all of you.

Since then, we’ve written 133,000 more words on the blog. In the past year, we’ve written blog posts the length of another epic novel (which I’m told is more than 110,000 words).

This also shows that we are remarkably consistent with our writing schedule. This year, we only missed one week of writing, and it was on purpose. We intentionally chose to not publish a post the week after George Floyd’s murder by police. We chose to shine the light on writers of color that week.

There are so many things that we’ve learned in the last year! One reason I love blogging is that it’s a great way to chronicle my own journey and mindset shifts. Writing also helps to solidify those mindset shifts for myself.

Here are a few important things we learned this year (which we will expand on below):

- We further articulated our beliefs about Slow FI. While we coined the term during our first year of blogging, we’ve continued to develop our perspective. This year we were able to articulate how gaining financial freedom can unlock different lifestyle designs.

- We officially became entrepreneurs. While Corey has had some entrepreneurial ventures in the past, I’ve only ever generated income from traditional (W2) employment. I launched my lifestyle design coaching during the quarantine this spring, and I’ve learned a lot through this process. I’ve built more of an abundance mindset and overcome a lot of limiting beliefs (although they creep back in every once in a while). Finally, we’ve started generating income that could grow to cover my (part-time) income by the middle of next year.

- We continued our Slow FI interview series into year 2. Because there are so many more inspiring stories to share, I expect we’ll continue it for years to come. We also started a new type of Slow FI interview this year. We started interviewing people who have retired early about what they would have done differently. Not surprisingly, many say they would have slowed down and enjoyed the journey.

- So far, we’ve survived the COVID-19 pandemic (and the other 2020 tragedies). I have been able to use a lot of the skills I learned to manage severe anxiety to continue to design a life I love even in the midst of the craziness. It can feel hard sometimes, but I’ve been able to cope and continue to work toward my long term goals.

This was a basic overview of a few things that have happened this year. To go a little deeper, I’d like to share my 10 favorite posts from year 2 of The Fioneers.

1. Why You Should Design Your Life Before Reaching FI

This is, by far, my favorite post that I wrote all year. When I first learned about financial independence, I thought that financial freedom was all or nothing. I was either financially independent, or I wasn’t.

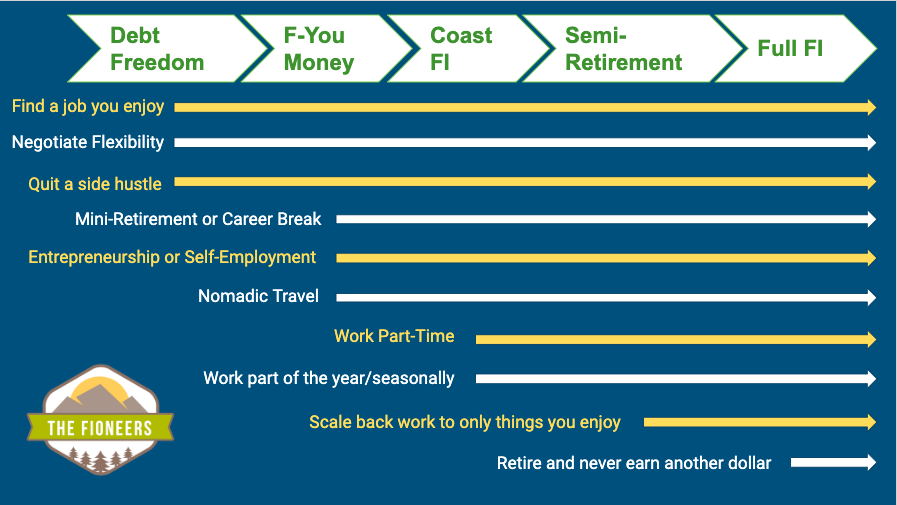

Now I realize that there are many stages that each of us will go through along our path to FI. These stages include debt freedom, F-You money, Coast FI, and semi-retirement.

Each of these new stages unlocks new lifestyle design options.

This is the post where everything that’s been swirling around in my head about financial freedom and lifestyle design came together. Financial freedom is not all or nothing. You can use the incremental freedom you gain along the way to FI to design a better life now.

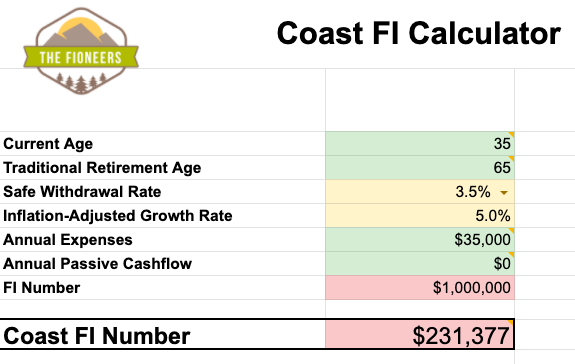

2. Your Ultimate Guide to Coast FI

The idea of Coast FI has been in the financial independence vocabulary for a few years now, but it has recently gained popularity.

Coast FI means that you’ve already saved enough for retirement. If you don’t add another dollar to your retirement accounts (and you don’t touch the balance), it will grow to provide you with a comfortable traditional retirement.

Coast FI provides you with three options:

- You can continue to save and invest. Every dollar you save is now contributing toward early retirement.

- You could decide to scale back on work and only cover your actual costs of living. Because you don’t need to invest more for your retirement, you can use the freedom to make our life better. You can find a better job, negotiate flexibility, start your own business, etc.

- You can land somewhere in the middle. You can continue to save, and use this new feeling of freedom to start making changes in your life.

For right now, we’ve chosen the third option. Reaching Coast FI has provided us a feeling of freedom that allowed me to make the decision to take a 50% pay cut to work part-time. We plan to scale back even more over the next couple of years.

FREE Coast FI Calculator

3. Why You Should Avoid a Two-Phase Path to Retirement

We’ve been inspired by many financial independence bloggers who have come before us. After reaching financial independence and retiring early, many have realized that FIRE isn’t everything they thought it would be.

Some went back to work. Others took years to recover from work-related stress and depression. Many wish they had slowed down along the journey because they are still generating income (that they don’t actually need) today.

I love this post that Corey wrote because it talks about the real risks of expecting that you can just “flip a switch” and be completely fulfilled in retirement. This is a well-documented concept, and a lot of pain and challenge can be prevented by taking an incremental approach.

Our goal is to make so many small changes along the way to FI. This way, when we hit our FI #, it’ll feel like any other day. We don’t need to change anything because we’ll already be living our ideal life.

4. How to Curb Emotional Spending

When I took a 50% pay cut to work 3 days/week, something really amazing happened. We spent significantly less money.

In the first year after I quit my toxic job and started to design my life, we spend $17,000 less. Even though we haven’t sustained a $1,500/month decrease in our spending over the long term, we have sustained a $1,000/month decrease over the last 18 months.

You might be wondering how we did it.

When we looked at our spending, we realized that decrease in spending fell into four main categories:

- Restaurants

- Groceries

- Travel

- General Merchandise

Not surprisingly, all of these could fall into what I’d call convenience and escape spending. When I was exhausted and burned out, we’d spend a lot of money on take-out and expensive, easy-to-make groceries. When I was miserable, we felt like we needed to enjoy the spoils of our labors. We took ourselves on luxury vacations, out to fancy dinners, and did a little too much retail therapy.

All that to say, we curbed our emotional spending. But, we didn’t do it by becoming more disciplined. We did it by addressing the underlying issues that were causing emotional spending in the first place.

This has created a virtuous cycle. We’re enjoying our lives more. This has reduced our spending riggers. We now spend less to make our lives bearable. Speaking less allows us to work less and enjoy our lives more.

5. Our Updated FI Plan

When we first started our pursuit of financial independence, our plan was to decrease our timeline and make sure that we still enjoyed the journey.

Now, our perspectives are quite different. This required us to make a new FI plan.

When we started on our FI journey two years ago (in 2018), our baseline timeline to reach FI was 11 years. Even with my decision to work part-time, two years later (in 2020) our timeline to reach FI is only 7 years.

Even though we focused a lot more on the journey than reducing our FI timeline, we still cut off two years from it. Part of this can be attributed to market gains. We attribute the other part to decreasing our spending and starting to generating income from side hustles.

Even though we could reach FI in 7 years if we kept everything the same as it is today, we aren’t going to. We plan to make more lifestyle shifts along the way that help us to align with our ideal life of becoming location independent.

We mapped out a new scenario that includes a transition to entrepreneurship within the next two years and a drop in our savings rate to 25%. Even with this change, we’ll still reach FI by 45.

Why would we wait to make shifts until we reach FI in 7 years?

6. Passion Hustle: The Fusion of Side Hustles and Passion Projects

Over the last year, I’ve had a significant mindset shift around side hustles. I used to eschew the idea of side hustles, especially when I was recovering from burnout. Why would I want to spend my precious free time doing something I didn’t enjoy just to make a little extra money?

Since then, a few things have happened.

- I’ve fully recovered from burn-out. When I’m not exhausted all the time, I find that I actually enjoy work, especially if it’s self-directed.

- I’ve done a lot of reflection on what my ideal life would look like if I didn’t need to work for income. It turns out, I can actually generate income doing those things. So, it doesn’t make sense for me to reach full FI before focusing on those things. Those activities might help me to be able to transition sooner.

As a result of these changes, I realized that there’s a lot of upside for trying to turn my passion projects into side hustles. My goal is that I can more than cover my actual expenses with them, so I can fully transition to a Coast FI and location independent lifestyle. Even if that doesn’t work, they could allow me to semi-retire years earlier than reaching full FI.

7. Seven Limiting Beliefs Every Entrepreneur Must Overcome

Now, I don’t want to give the impression that launching a business is easy. When I first launched my coaching business this spring, there were so many unexpected things that I didn’t know how to do. I didn’t always understand how to respond to challenges or how to adjust course.

On top of all of this, limiting beliefs were coming up left and right. Limiting beliefs are internal barriers that can hold us back from accomplishing our goals.

Limiting beliefs could include things like:

- I have to do something perfect the first time, or it’s not worth doing.

- If I don’t know it’s going to be successful, why should I put time and effort into it?

- I should be able to figure this all out by myself.

- I need to feel totally confident before moving forward.

These are the kinds of limiting beliefs that can hold any of us back from making progress toward our goals. I feel lucky to have had such great support to work through these challenges. This support came from a coach and an accountability partner who is launching her own coaching business.

Whenever you take a step toward any goal, limiting beliefs will come up. It’s important for us to recognize them, to have strategies to work through them, and to have a community of support.

8. Coast FI: A Better Path to Financial Independence

I’ve always been fascinated to hear the stories of people who retired early so that I can understand what they would have done differently. It’s so important to learn from the mistakes and regrets of those who have gone before us.

This year we decided to start a new type of Slow FI interview. In this new type of interview, we share the stories of people who have retired early about what they would have done differently on their path.

The first interview of this type was with Robert from Stop Ironing Shirts. I first got interested in Robert’s story after he wrote a post earlier this year about how he wished he had scaled back earlier and taken a Coast FI approach.

Looking back, he realized that he made a ton of sacrifices when he didn’t need to. He didn’t realize the financial freedom that he had already gained would have allowed him to make decisions to improve his life along the way.

9. Why You Shouldn’t Ignore Active Income

Since starting the Slow FI interview series, I’ve been searching for someone who actually took a semi-retired route.

To me, semi-retirement means that you start to withdraw funds from your portfolio. And, you still need to generate some active income to cover the difference.

A lot of people call themselves semi-retired but don’t actually fall under this definition. Some have already reached FI and are still generating income. Of these, many still cover their full annual expenses with active income. Some are actually what I would call Coast FI. They are still working part-time, but they are actually covering their full expenses. They might feel semi-retired, but they aren’t yet pulling from their investments.

You might be wondering why this even matters. It mattered to me because I’ve considered us taking a semi-retired approach one day.

It also seems like people who pursue financial independence sometimes have a hard transition. It’s scary for people to go from saving more than 50% of your income to withdrawing money from your portfolio.

This is why I loved the interview with Rebecca and Joe. They actually decided to quit their jobs 2-3 years earlier than they originally intended. Earlier this year, they were introduced to semi-retirement. Based on this understanding, they realized they could quit early and would only need to generate up to $8,000/year in active income.

10. How to Cope (And Hopefully Even Thrive) in Times of Disaster

This wouldn’t really be a reflection on 2020 if I didn’t talk about the COVID-19 pandemic. As much as this has been hard, it is one of the first times in my life I felt lucky for having dealt with severe anxiety.

It’s been such an extreme situation that everyone is feeling it. Many people who had never experienced anxiety in their lives were all of a sudden thrown into a situation where they had no idea how to cope.

Given my experience with anxiety and other mental health issues, I realized that I was well-equipped to handle it. I was able to tap into all the same strategies that I had used to manage the severe anxiety I’ve experienced in the past.

The main difference was that this was actually something scary (not just something my mind thought felt scary).

Earlier in the spring, I also had the opportunity to run a live workshop to share these strategies with our community. I also did a few podcasts interviews on the topic and shared the insights in a live session in the Choose FI Facebook group.

It felt rewarding for me to be able to share the things that I’ve learned. Some good things have ended up coming out of the crisis and mental health issues I’ve experienced, and this is one of them.

Looking Ahead to Year 3

A lot of things in our world are uncertain right now. Who knows what will happen in the next 12 months? What will we write about in the next 133,000 words on our blog?

Here is what we do know.

- We will continue to write weekly to share things that we’ve learned (and are learning) with you.

- We will continue to amplify the stories of people who’ve chosen to design their lives along the way to FI through our Slow FI series.

- I will continue to build up my passion hustles in a way that will help me reach my long-term goals in a way that helps me live as close to my ideal life as possible. (The journey should be as remarkable as the destination)

Here’s what I’d love to see happen in the next year.

By this time next year, I’d love to be a “full-time” entrepreneur. For me, this means that I won’t need to do any W2 work. I’d love to generate a full-time income working part-time hours as an entrepreneur.

Even if this doesn’t happen by 2021, it’s something I’m aspiring to. I’ll definitely be sharing more over the next year on the blog about what it’s like to build a business and making a transition to entrepreneurship.

I’m expecting that COVID will still be an issue throughout the duration of 2021, so we are planning accordingly. We’d love to travel around the USA someday in an RV or campervan, so we’re looking to experiment with this. Next summer, we’re planning to rent a campervan for an adventure. We’re excited to see if #vanlife (at least for certain periods of time) is for us.

Last year, we started our minimalist journey by doing a minimalist challenge. We got rid of 500 items in a month. This wasn’t enough. We’ve accumulated too many things over the years, and after all the time spent at home during the pandemic, it’s starting to stress me out again. I expect you are going to hear a lot about minimalism from me over the next year.

Also, over the next year, I’d like to dive more deeply into what it means to have an abundance mindset vs. a scarcity mindset. I definitely have a tendency toward a scarcity mindset. I’ve worked through many aspects of this over the last few years, and I still have a lot of work to do. I’m excited to share with you what I learn along the way.

Here’s to Year 3 and 133,000 more words! I can’t wait to see what it brings.

FREE Coast FI Calculator

Congratulations on year 2! I enjoyed the reflection and seeing your evolving thinking on financial independence. As we are getting close to FI, I’m starting to shift my thoughts on what the next few years will look like. I don’t think I’ve gotten quite clear enough yet, but I’d love to have it this clearly laid out by my 2 year blog anniversary.

Looking forward to year 3!

Hi Ed,

Thanks so much for your comment! I’ll look forward to hearing more about what you want your life to look like as your approach FI!

Best,

Jessica

Thank you for taking the time to share your thoughts and lessons learned! Looking forward to more this next year.

Jessica,

Jenni and I were just reading your 10 Questions post over on 1500 Days and catching up a bit on your experience with this second year review. Great job! Jenni could certainly relate to gluten concerns and love for cider (she’s celiac). One of our favorite cider-related experiences was hiking Dartmoor in England after visiting a literal farmhouse to pick up a very large container of farmhouse cider. We filled our hydration bladder in our hiking bag with what was probably a gallon of cider and set off for our hike to several cairns. Gorgeous!

I really like your flexibility in your approach, a willingness to reevaluate and adjust. I think that’s healthy. I was curious about word counts once I saw yours and noticed we just crested 90K starting since May of this year (!!); it’s nice to have a creative outlet and somewhere to document your experiences whether it’s a blog, journal, or other place. Wishing you the best with your entrepreneurial steps and hoping you’re careful not to cannibalize any hobbies for the sake of money. Be protective of the things you care about: money can *sometimes* infect them in a negative way.

Cheers!

Hi Chris,

Thanks for your comment! I appreciate the thoughts around cannibalizing the hobbies for the sake of money. Ultimately, I think I’m mindful enough to know if I want to be doing something or not, so I’m hopeful that I’ll be okay. Especially since I don’t have the goal of generating a crazy amount of income. I’m good with whatever it generates – I just suspect it’ll be enough to allow me to quit my job. We’ll see! 🙂

Thanks,

Jessica

Seriously long post. The one thing stood out is that cutting spending over longer term is harder than expected.