I am excited to bring you a new type of Slow FI interview. Up to this point, the Slow FI interviews have all featured people who have intentionally chosen to utilize their financial freedom along the way to FI to improve their lives.

This new kind of Slow FI interview is from someone who already reached FI and was willing to share what they would have done differently along the journey. There are so many people who have reached FI who can provide us with incredible insights about the approach to take. Many of them wish they had taken a slightly different approach, often wishing they had slowed down to enjoy the journey along the way.

For the first interview of this new type, I decided to interview Robert who writes the blog Stop Ironing Shirts. Several months ago, I read a post he wrote about Coast FI.

Coast FI is when someone already has enough invested in their retirement accounts that would grow to provide them with a comfortable traditional retirement. They wouldn’t need to add another dollar. If someone has achieved Coast FI, it means that they only need to cover their actual costs of living with active income.

This post was a reader question that asked if they should coast to FI or pursue early retirement. Robert, who had recently retired early, recommended Coast FI and shared that he’d wished he’d taken that approach himself.

After reading that, I knew I needed to reach out and learn more about Robert’s story! That discussion turned into a request for a new type of Slow FI interview.

Let’s get into the interview.

1. Tell me about you.

My wife and I are elder millennials (born 1982). We are financially independent. I quit/retired from my job in finance in April of 2019, and my wife stopped practicing veterinary medicine in 2014. We are just under a year into living our financially independent/retired early lives and the coast in South Carolina is our new home (for now).

2. Why did you decide to pursue financial independence in the first place?

The short answer is financial security. My parents married young, had me when they were 23, and subsequently divorced. Both of them came from what would be considered traditional households. Their parents had college degrees and were married for 40+ years. My parents chose a different route.

I lived with my mom and her second husband, who would be best known as a former free spirit. There were constant money problems at home. My mom liked to spend money but didn’t like to work. She was fully capable, but working wasn’t her thing, especially after the booming restaurant she worked at part-time shut down when I was 13. My stepdad worked hard but was limited in how much he could earn with minimal job skills. He also wasn’t always the most urgent individual.

I had a limited relationship with my dad, who eventually started earning a decent living in my teenage years. He, however, had other financial pressures (i.e.new spouse plus additional child support).

I started putting the correlations together in my teenage years:

- Working = Money

- Not Working and Spending = Not Having Money

- Not Having Money = Stress

I had the benefit of a large extended family. I got to see the difference in lifestyle and stress levels between those who worked more and spent less and those who worked less and spent more. Seeing these differences were responsible for my early money mindset.

As I was nearing the end of high school, I got rejected from the college I wanted to attend. So, I then chose the next school based on cost. I worked while I was in school, graduated in three years, and took the “safe” job offer in a training program for a large company.

I began to actively learn about money during college. I attribute my early interest in personal finance to my formative experiences. I didn’t know about financial independence yet. I just knew that savings and investing were good while spending money negatively impacted how much we could save and invest.

It also helped that I met my wife early in college and we got married at 22. She was naturally frugal, even more so than me. We spent just over three years together in a nice mountain town while she was in graduate school. My take-home pay was just under $30k in the mid-2000s and we could live on that amount of money and have a pretty good life. Most of our entertainment options were free/outdoors, and I think that avoided the lifestyle creep.

3. How did you approach your FI journey? What levers did you focus on?

In the beginning, our FI journey was savings focused. My earnings were capped early in my career due to limited opportunities in the area and my spouse being in school.

We moved to a big city at 25 and both started working professionally. At the same time, we didn’t see our spending go up substantially. She got a job offer at $50,000 and my pay increased to $60,000 by moving to the bigger city. The increase in our incomes combined with not increasing our spending started us down the path to FI.

The first nine years of our FI journey were 100% savings focused. Her income as a veterinarian was capped. I was working as a small business banker. This was during a time where bankers were being laid off or their employers were being shut down by the FDIC. I carried with me a constant fear of unemployment.

I ran a few calculators that told me that we might be able to retire before I could receive my pension at 55. One even said I could retire by 40, but I never thought it was much of a reality.

We turned 30 in 2012 and had a $323,000 net worth to show for my 9-year career and my wife’s 5-year career. It could have been higher, but three things worked against us:

- Student Loans: We had just over $100,000 combined that we were chipping away at.

- Buying a House Before the Market Bottomed Out: We made the mistake of buying a house in 2007. On top of that, we bought one that was far too big for our needs and too far away from the city center. We paid $255,000 and at the depths of the market, it was only worth $170,000. Being $84,000 under the purchase price of a house within a couple of years was eye-opening. The psychology of “being underwater” caused us to force a lot of savings into the mortgage instead of investing in the market.

- Recession Market Returns: The market returns were pretty paltry at the same time our income/savings were increasing. 2007 to 2012 were rough times to be invested in the equity market.

Our finances shifted quickly after 2012. My job status in my employer’s eyes went from “He should just be thankful not to be laid off” to “high demand employee”. Coworkers who had delayed their retirement by 3,4,5 years finally retired and there was suddenly a lack of talent.

My base salary went above $100,000 and annual bonuses increased. The struggling practice my wife worked for started doing better, and she got her first pay raise in three years. In 2013, the market returned 30%. Those three things combined increased our net worth by over 50% in a single year.

In 2013, I stumbled across Mr. Money Mustache. His blog made us rethink the idea that we were destined to always work. We then began to examine some slow leaks of money in our budget.

We were faced with a number of questions now that we suddenly had money, flexibility, and options. We considered:

- Buying a different house to shorten my commute (We made an offer but didn’t get it)

- My wife quitting her full-time job to pursue something part-time

- Getting into real estate investing (I overanalyzed all of the great deals, and we ended up not pursuing it)

- Pursuing a promotion and relocation with my company

At this time, there was *zero* information out there talking about Slow FI. I wish there had been more people talking about all the different options. I was just looking at “If our spend rate is X, here’s how much we need to save”. At the time, I didn’t fathom the ability to earn more money after leaving my profession. It was either work full-time as a professional or don’t work at all. My mind was tainted by the terrible employment market in the years prior.

After 2013, we shifted our focus to earning more. First, we elected to relocate and move eighty miles for my job. I took a small promotion, and my wife took a career break. This promotion was for an entry-level leadership role where the compensation was capped around $150,000-$160,000.

Ten months later, my work asked us to move again. This time, we moved much further – 850 miles – away. I took that opportunity because it was much higher pay. For this job, I was able to negotiate compensation that was double my previous pay through a combination of salary, bonus, and other incentives. My compensation continued growing steadily in my last four years of working. I ended up earning $327,000 in my final year of employment.

4. When did you reach FI? Was that timeline different than you originally thought?

We reached what I’d consider full financial independence sometime in 2017. Our normal spending of $50,000/year would be covered by the 4% rule from our investment portfolio.

When we found financial independence in 2013, I calculated it would take roughly four years to become financially independent. After reaching FI in 2017, I continued to work until March of 2019 to add some additional layers of security into our FI plan. Part of the additional time worked was driven by bonuses, stock vesting, and pension milestones at my employer.

5. Was there anything that happened along your journey that shifted your perspective about FI?

There were two moments that stick with me in the latter part of our FI journey.

In late 2014, I had finally relaxed and didn’t feel as much stress about scarcity and not being employed. I had just moved and taken a higher paying job and the company started another round of layoffs. I again thought my job had the possibility of being eliminated and I was extremely stressed and not sleeping well.

Eventually, I realized that we had enough F-You money. We had sold our previous house, received the equity, and only put 20% down on the next house. This meant we had over $100,000 saved outside of our retirement accounts. This could provide us with two years of living expenses. Realizing this was a huge weight off my shoulders. The worst-case scenario was that I would need to get a nominal job and ride a bike around town, but we wouldn’t starve. In hindsight, I wish I could get those sleepless nights back.

The next moment happened in late 2016 and 2017. This time was especially tough for us due to my wife’s health. She got a persistent headache along with other mysterious neurological issues after a normal workout in November of 2016. Things got progressively worse, and it started a long and painful health journey.

Suddenly, much of the life we expected to live was in question. We could never get a clear answer about the diagnosis, treatment options, or recovery plan. Money and career was suddenly an afterthought.

This was our new priority. I no longer cared if no work fired me. I could not put in 100%. They could have 40-50% of my time or none.

We spent thousands of dollars to travel across the country to see specialists at teaching hospitals and try different procedures. Money became a much lower priority, especially as I learned about the struggle of other patients.

We reached FI during this time, but I really couldn’t tell you the date. It was an afterthought to the primary issue we were dealing with. My professional identity and money wouldn’t matter if I lost my spouse at 35.

This period of time was especially bad for us. My wife underwent multiple procedures that ultimately fixed the issue with her spinal cord in July/August of 2017. The recovery process has been measured in months, quarters, and years. We are now grateful she is living a normal life and managing only a few minor residual symptoms.

If you knew then what you know now, what would you have done differently on your journey to FI?

I am proud of our FI journey, but if I could go back and do things differently, I would have taken time in 2013 to consider Coast FI.

Coast FI is when you have enough money invested that you could have a comfortable traditional retirement, as long as you don’t touch it and let it grow. When someone reaches Coast FI, they only need to cover their actual costs of living. At this point, we could have scaled back work to make $50,000/year to cover our expenses.

To be honest, I may or may not have chosen this path at that point. I was 31 years old, and I still felt like “there was something to prove.” Looking back, I wish I had slowed down.

For me, Coast FI would mean still using my professional skills but doing so at either a lower stress employer or in a part-time capacity. I differentiate Coast FI from the term “Barista FI”, which I think implies moving from a high-paying, high-skilled job into a lower-skill, lower-paying job to supplement retirement income. If I still need to exchange my time for money, I want to do it at a high rate. In my profession that would have looked like me working for a more relaxed community bank, where people in my position average 30-35 hours a week.

We had the financial capacity to pursue Slow FI, but we never considered it. In hindsight, I know why. We went from feeling like we had no options up until 2012 to endless options in 2013, just one short year later. In 2012, we had poor market returns, an underwater house, and lukewarm job prospects. In 2013, all three changed, and it was hard to wrap our heads around.

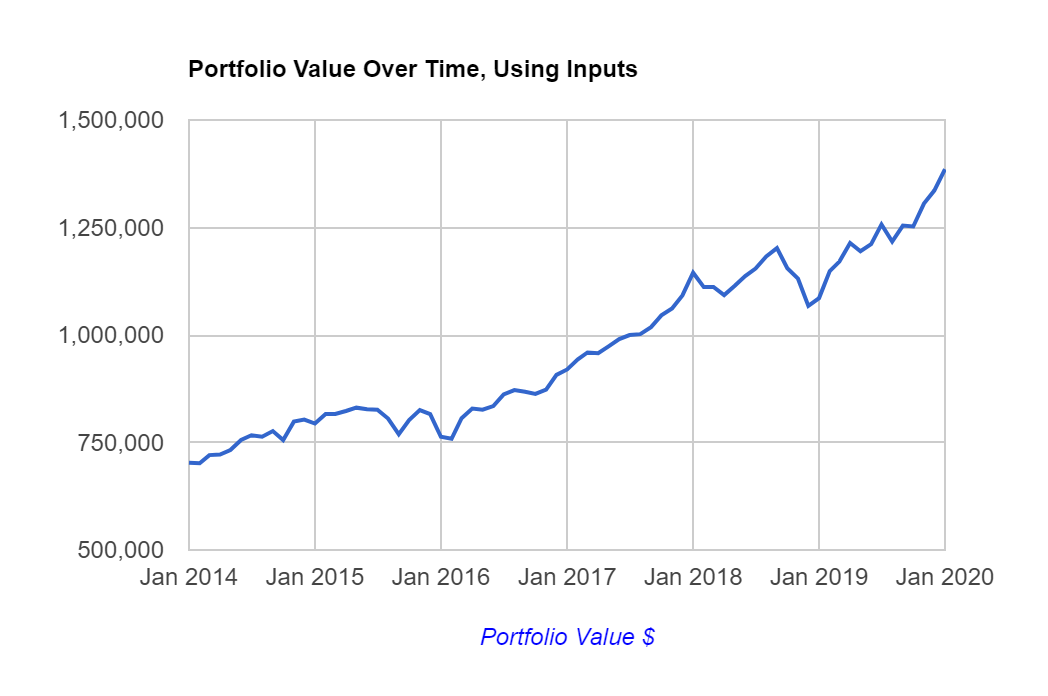

Let’s talk about the numbers. We had $703,000 in net worth at the end of 2013. If we had taken a Coast FI route and not added any more money to our investments, they would be worth $1,385,000 at the end of 2019. This is surprisingly close to our baseline FI number before accounting for any money we saved after 2013.

In 2013, I could have taken a lower stress job. We could have strategically relocated with my company to an area we wanted to be! Instead, I chose to move to Dallas-Fort Worth, 850 miles away from family and from the outdoor recreation we enjoy.

I gave away almost half of my 30s to a high-stress job in exchange for money that we didn’t actually need.

We also got mired into our jobs for so long that we delayed important discussions about life goals and having a family. Neither of us expressed an interest in having kids in our 20s. We were too focused on our careers.

Looking back, our thoughts about it started shifting around the same time, but we never talked about it. At the time, continuing to do the same grind was easier than slowing down and having the tough conversations about what we wanted. That goal has eluded us, and in hindsight, I realized that I gave my time, efforts, and life energy to my stressful job rather than having important conversations.

The last thing is that I wish I would have focused more on what could go right instead of what could go wrong. I delayed quitting my job for almost a year because I thought too much about the “what if” scenarios. What if health insurance costs increased? What if the market returns were lower? What if the 4% rule isn’t enough?

These were delay tactics, and I needed to overcome my fear to take the leap.

7. What has happened since you retired early? Have recent shifts in the economy changed your perspective?

Before I quit my job in 2019, our savings were front-loaded. Between stock vesting, the annual bonus, and 3 ½ months of salary meant we still achieved a 50% savings rate for the year. All of our investments were made in the first quarter of 2019. In the year between quitting my job and February of 2020, our portfolio rose another 15%.

I also ended up with a “job” using my skillset to help a friend’s company on a part-time and remote basis. I was originally volunteering to help, and later they decided to pay me. This alone covered 40% of our expenses, so we didn’t need to pull as much out of our portfolio.

Unfortunately, this was short-lived. In March of 2020, the company encountered COVID-19 related struggles, and they had to furlough my position. While we did lose money in the market downturn, we are still financially independent but on the leaner side (floating between 20-25x our annual expenses depending on the market).

I expect my flexible working arrangement will come back eventually, but it will likely be 2021 before their business is past this crisis.

So what does this all mean for us?

I’m still proud of the path we took and the things I accomplished in my career. At the same time, all of these experiences have motivated me to push others to consider all of their options, including the Slow FI approach.

I would encourage people to build up skills that are valuable. Then, they can work fewer hours at a higher hourly rate. If I end up needing to earn money in the near future, there are temporary assignments available in a couple of different related fields.

Independence and freedom come from both financial resources and a strong network and skill set. If our financial resources fall below the point where work is no longer optional, I’m confident I can find paying work at a rate in excess of our living expenses.

I’ve now talked to a number of people who’ve done the tough part, saving well and building skills for the first decade of their careers. If you’ve built a strong foundation in our 20s and 30s, you will reach financial independence eventually.

The question to consider is: What kind of life do you want in the meantime?

Thank you, Robert, for sharing your story with us!

I really identify with this story. While I am about 5 years younger than Robert, I also identify with not having a lot of job (or life) options early in my career. I also didn’t make a lot of money, but I didn’t spend a lot either.

It’s interesting that Robert shares that it felt like financial freedom snuck up on him. Over the course of a year or so, he went from having few options and little financial freedom to having a wide variety of options. Since he was so hard-charging in his career, he didn’t stop to take a breathe and get a sense of what new opportunities would be available for him.

In some ways, I feel the same way. I was also very career motivated. After 10 years in my career, had I not experienced my anxiety issues, I may have continued pressing toward full FI. Looking back, I am thankful for the experience because it required me to step back and reconsider my life and my goals.

For Robert, this perspective-altering event didn’t happen until his wife was experiencing significant health challenges. It’s amazing how crises can expose how much we invest in our careers rather than the rest of our lives.

A few weeks ago, I asked Robert if he had changed his perspective on Coast FI now that we’re in the midst of this pandemic. I was somewhat surprised to hear him say that he feels like making sure people know about Coast FI is even more important now.

I agree. If I was still pursuing full early retirement, I might be devastated by this situation because I would believe that I needed to now stay in a job I didn’t enjoy for longer. Because I’m working on building up a business and working part-time, I feel a lot more confident in my financial situation. Having a stable job that I enjoy helps me to have more confidence in my financial situation during this crisis.

If you want to learn more about Robert’s story, you can find him in the following places:

- Blog: Stop Ironing Shirts

- Twitter: @stironingshirts

- Instagram: @stopironingshirts

Great to learn more about your story! We are about the same age and we can’t help think about if we did things differently. Hopefully you are enjoying the times now as you settle into your new life.

Glad to hear your wife is doing better after the medical issues. That sounded like a scary situation.

Thanks for sharing this.

There is always a balance between planning for tomorrow and living like there is no tomorrow.

Of course, some things will always be out of our control, but being financially literate and responsible and aiming for FI gives us more options than not.

Hope you are doing well

Shaun

Hi Shaun,

Absolutely. I’m so glad that you enjoyed the post. Robert did such a great job with it.

Thanks,

Jessica

Is there a coast/slow FI calculator?

Hi Spencer,

Yes, you can find the Calculator in this post: https://thefioneers.com/financial-independence-milestones/

Best,

Jessica

I’m late to read this one, but I’m grateful I took the time. This is a fascinating look into Robert and his wife’s story and I feel like we’re sort of following in their footsteps, just half a decade behind.

I like to be fairly conservative with our numbers, and I think I can say now with some level of confidence that we’ve reached our Coast/Slow FI number and it’s now a matter of when do we decide to scale back. . . or do we push through and reach FI?

I still don’t know the answer, but more and more I find myself leaning toward the former.

Hey!

Thank you so much for the comment. Robert did a fantastic job with this interview. Congratulations on reaching our own Coast FI number. Just remember, it’s not an either/or. It’s a both/and. You can both reach FI and live an awesome life along the way. It might take a bit longer, but you won’t care if you are loving life!

Best,

Jess

Loved this story and I resonate with it a lot. FI snuck up on me as well. As I worked towards it, I thought it would be a monumental event where I’d hit a specific number and fireworks would go off in my head. Instead, it was more like, “oh wait, I think we’re FI now”….

Thanks for sharing your story! I definitely think that if people aren’t super intentional about it, it definitely sneaks up on you!

Jesica

Just found your site and it really resonates with me. I’m coast FI but finding it difficult to stop contributing to my investment accounts. I want to do so to build up my Cash to allow more freedom, choices, opportunities, maybe a vacation home 🙂 Can you lead me to any posts regarding this? So hard to transition from saving/investing and somewhat of a scarcity mindset to abundance.

Hi Rainee,

Congrats on reaching Coast FI! The power of coast FI is that you don’t need to stop contributing, but you get to choose how much you want to contribute now if any. And, if you want to keep saving, the money can go toward other goals!

I’d definitely recommend a recent post about financial metrics that can help us build an abundance mindset. Here’s the post: https://thefioneers.com/financial-metrics/.

Best,

Jess