Financial independence is as much about the journey as it is the destination. And while we are still years away from arriving at our intended destination of FI, we have a financial independence plan that is about both the journey and the destination.

This post focuses heavily on the finances of our plan to reach financial independence, but that is not to suggest that the journey to financial independence is all about numbers.

This post was originally published four years ago, and then updated two years ago. Similar to our last update, a lot has changed in the past two years. It feels appropriate to share an updated plan with all of you.

Many (if not all) of the core principles have stayed the same over the course of the two years. This has been remarkable to confirm. And thus, why we’ve chosen to refresh the original post, keeping most of the original content (as a comparison) and adding new elements that better describe our plan.

It also seems fitting that when we first published this post, we made the following two clarifications.

First, this plan is NOT written in stone. Let’s face it, life just isn’t that simple. We learned this lesson the hard way just months out of college and weeks after we got married.

Three weeks after we got married, Jess and I moved to Nicaragua to teach English. We intended to stay there for at least a year, only to return 6 weeks later, each of us twenty pounds lighter after three life-threatening bouts of various illnesses.

Needless to say, life did not go as planned. And we learned that the hard way.

Plus, the only thing that I know that is written in stone is a tombstone, and I’m not done living yet. Writing a master plan that wouldn’t change over time would be like writing our tombstone.

I’m not in a rush to do that, but I did have a little bit of fun with some free tools found on the internet. See below.

Second, our plan is also NOT the shortest route to financial independence. Imagine you’re planning a traveling vacation with the primary goal being to have an adventure and to see new sites. How do you go about this plan?

Do you pick the shortest route to go from site to site, or do you plan it out with stops and detours to make the most of the trip? I think hope everyone is likely to answer the latter.

Yet somehow not everyone takes this approach when pursuing financial independence.

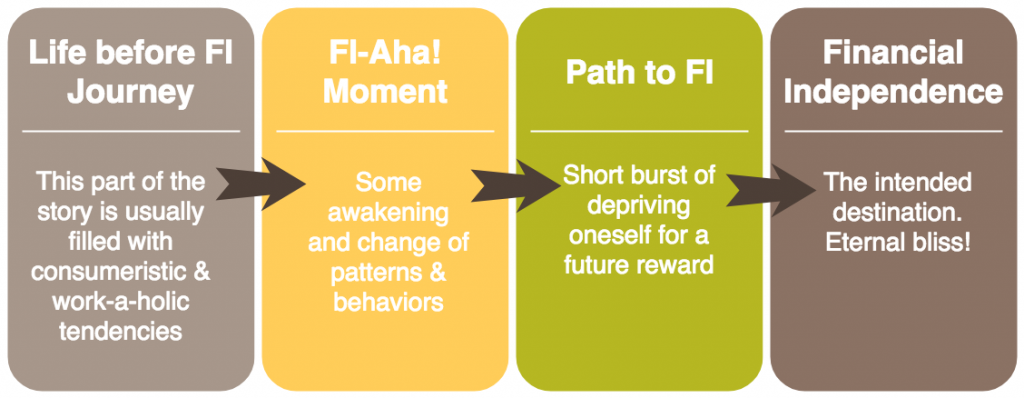

Too often FI narratives are filled with words of endurance, often suffering at a job that they hate, only so that they can enjoy life later.

In these stories, these fioneer pretenders are so focused on getting to financial independence (as some mystical destination), that they forget about the journey to get there. These individuals not only lose sight of the lifestyle that they hope to create after reaching FI, but they run away from it.

Here’s what a common path to FI looks like:

These stories can still be inspiring. But what this typical approach fails to anticipate are the sudden life changes that are likely to come when they reach financial independence.

People who think that lifestyle changes can happen with the flip of a switch, making sudden leaps from one phase of life to another, are sorely mistaken. There are moments to make drastic life changes, but my point is that often these notable changes are filled with smaller decisions along the journey.

Our plan to reach FI is not to deprive ourselves to build up a nest egg so that we can relax later. And to be clear, our journey to financial independence is not about early retirement. We are not looking to not work or sit on a beach for 50-60 years. Instead, this journey is about lifestyle design, freedom, flexibility, and security.

We plan to take very intentional actions so that we can adjust our lifestyle along the way. Here’s a detailed look at what our plan looks like.

Wow! Those two clarifications are as true today as they were four years ago. We’re excited to share with you how much we’ve learned and how much our plan has shifted.

Our Financial Independence Plan: Where We Started 4 Years ago

Before we jump into HOW we will achieve financial independence, it’s crucial to better understand WHERE we started our journey four years ago.

Four years ago when we started this journey, we didn’t start from zero. We had jumpstarted our pursuit of financial independence with intentional lifestyle decisions. That’s not to discourage others from doing the same thing – it just means that we had been saving a few years. It wasn’t day 1.

Our Original Baseline Numbers

This is where we were four years ago when we made an intentional decision to pursue financial independence:

- Age: We were both 31 years old.

- Assets: We had 4-5x our annual living expenses currently invested in the stock market, excluding equity in our home and additional cash reserves.

- Savings Rate: We saved 57% of our take-home pay that year. Increasing our savings rate was a major focus for us then.

- FI %: We were able to cover approximately 15-20% of our annual expenses indefinitely by using the dividends and appreciation from our portfolio without depleting our assets (using a 3.5-4% safe withdrawal rate).

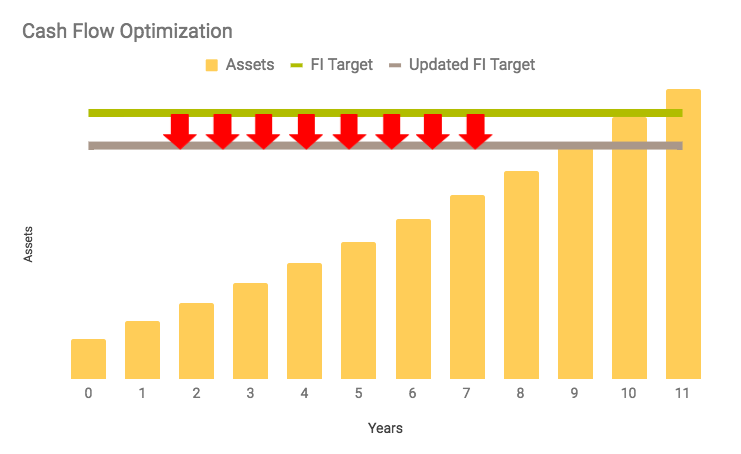

Based on our savings rate and assets at the time and a few other assumptions about market performance, we calculated that we would reach financial independence in 11 years.

One part of our plan was understanding our baseline. In other words, if we made no changes to income or expenses for 11 years, we would reach financial independence by the time we were 42 years old. As we stated early on, we knew it was unlikely that we’d make no changes, but it’s helpful from a planning standpoint. Here’s our original chart:

We were really motivated by this baseline. Reaching financial independence in our early 40s seemed like a big accomplishment.

At the same time, it was hard to wait for 11 years. When we first published our plan, we were at a critical milestone for Jess’s career. She was working in a toxic work environment and ended up taking 6 months off to overcome severe anxiety.

I remember when we realized that Jess literally could not last another week in the toxic work environment, let alone 11 years. For that reason, we mapped out multiple strategies and scenarios to optimize our plan from a financial standpoint, while leaving room for lifestyle changes we wanted to make.

Our approach was very clearly articulated with these words:

Our Plan to Reach FI: to quicken the pace to reach financial independence while aligning our values with our spending.

Our Original Financial Independence Plan (4 Years Ago)

Our original plan to get to financial independence, from a financial perspective, was focused primarily on:

- Decreasing our expenses

- Increasing our income

Decreasing Our Expenses

New to the pursuit of financial independence, we wanted to optimize our spending. We were spending money in many areas of convenience and for items that did not align with our values. We understood this and prioritized this early on in our journey.

Four years ago we set a goal of decreasing our expenses by $10,000 per year.

Decreasing our expenses helps us two-fold. First, it allows us to save (and invest) more money, which will contribute towards our other goal of wealth accumulation, but more importantly, it lowers the amount we need to save to reach financial independence.

I’m going to say that again because this is critical to our success.

By learning to live on less, we not only have more money to build up our nest egg, but we will require a smaller balance to consider ourselves financially independent. The nest egg will have to fund a less-expensive lifestyle.

Here’s a visual that helped articulate how our goal to decrease our annual expenses by $10,000 would impact our journey to financial independence. We estimated that by decreasing our annual expenses by even $10,000, not only will our assets grow at a faster pace to allow us to hit our original target 1 year earlier than our baseline, but the target decreases so that we hit our updated FI target another year earlier, in year 9.

Our plan to decrease our expenses included the following strategies:

- Lower our groceries bill by $500 per month and eating out less often

- Use credit card reward points to minimize travel or vacation expenses

- Buying less stuff and curbing emotional spending

Our intentional shifts over for the first two years of our FI pursuit years worked. Two years ago, when comparing our spending from that year to two years prior, we were spending approximately $12,000 less per year.

We have learned two important lessons about spending. First, everyone has different spending triggers, but focusing on food, not paying for convenience, and using travel hacking really did make that big of a difference for us. Second, you can’t be afraid to spend money where you value it – but should do so intentionally.

Increasing Our Income

The other side of our plan was increasing our revenue. While this won’t have the same dollar-for-time impact on our path to FI, this was also part of our plan because of the limitless potential.

While we can only decrease our expenses so much, there are theoretically no limits on how much money we can make.

Once you remove the mental barriers and stigma for earning more money, you’ll be amazed at what you can do. Increasing our income has been a big part of our success.

Our goal four years ago was to find a way to increase our income by $20,000 per year in the first two years. If we were able to accomplish that, here’s what it would do to our timeline to financial independence.

While it may look like the FI Target and Updated FI Target decreased from the previous scenario, this is not the case. The dollar amounts represented with each of these lines stayed the same.

The yellow bars, representing our wealth accumulation, grow at a faster pace. This is intuitive. The more money you earn and can save, the faster you can build wealth.

There were three primary ways we planned to increase our income on our journey to financial independence:

- Increase our W2 Income

- Build up a side business

- Increase our Real Estate Income (originally planned for 2019)

Spoiler alert. Four years later, we have not yet started investing in real estate. Originally planned for 2019 got pushed to 2020 because of other competing priorities. Then COVID-19 happened, and we have decided to move away from real estate investing in the near term (and likely forever).

Growing our income has been successful, but not how we originally planned. I was able to increase my W2 income, and we started making money from our side hustles.

What we didn’t plan for just four years ago was Jess returning to work part-time or her quitting that part-time job to take The Fioneers full-time.

Shortly after first publishing this plan, we found ourselves at a crossroads. Return to working full-time and risk Jess’ health taking a turn for the worse, or extend our timeline to FI and enjoy the journey.

Given our emphasis on the journey and priority to Jess’ health, it was really an easy decision.

This decision was made easier knowing that I was increasing my income, and we were decreasing our expenses. Jess taking a pay cut would only extend our timeline by a couple of years, or so we thought.

This was the lifestyle change that, in large part, inspired Slow FI.

After having another two years to reflect on this lifestyle change, this change has been one of the best decisions of our life. It not only provided Jess with a better balance but gave her the freedom to invest more time into getting the business off the ground.

Now almost 4 years from the original publish date, Jess has had about 1 full year of working for herself full-time. And we continue to thrive. We did not expect these decisions to lead to higher incomes. But, last year was one of our highest income years ever when we combined my higher W2 income and the business revenue.

Our Financial Independence Plan 2 Years Ago

When we first updated this post, I remember thinking how enjoyable it was to compare where we thought we would be and where we were (2 years after the original publish date), on our path to financial independence. As a reminder, here’s where we were two years ago.

Our Numbers as of 2 Years ago

Here’s a look at our numbers.

- Age: We were both 33 years old. (Shocker, I know)

- Assets: We had 7x our annual living expenses currently invested in the stock market, excluding equity in our home and additional cash reserves.

- Savings Rate: That year we saved 58% of our take-home pay.

- FI %: We were able to cover approximately 30-40% of our annual expenses indefinitely by using the dividends and appreciation from and without depleting our assets (using a 3.5-4% safe withdrawal rate).

Based on the savings rate and assets from two years and a few other assumptions about market performance, we calculated that we would reach financial independence in 8 years.

I know, I was a bit shocked too. Especially considering the decision to have Jess work part-time. Please note – in this stage, she was still working her part-time job and we weren’t really earning income from the business.

Between 4 years ago and 2 years ago, we managed to shorten our timeline to financial independence by one (extra) year. That is a result of three things:

- The stock market had a strong year 3 years ago (well above our estimated 5% inflation-adjusted estimate)

- We had decreased our expenses significantly

- We started to make a little money on the side

Here’s a visual of our updated timeline to achieve financial independence (from two years ago). Again, this assumed that everything would stay the same for the next 8 years.

Our Financial Independence Strategy 2 Years Ago

Our strategy for reaching financial independence had also changed. We were no longer looking to quicken the pace to reach financial independence.

Instead, our priority had shifted to design our ideal life while continuing to pursue financial independence. If we could maintain the pace while making incremental lifestyle changes, even better. But, we didn’t need to.

As I mentioned earlier, one of the strategies for gaining financial freedom and reaching financial independence that we have been considering is real estate investing. This was one of the reasons we decided to do a cash-out refinance in 2020.

It provided access to cash that we could use to purchase a rental property. Our main reason for doing this is that the mortgage on our primary home would be at a better rate than financing a rental property.

We had been thinking about buying a rental property for several years. In addition to the refinance, we have been saving for this goal for a few years. This means that in 2020, we had a large amount of cash sitting in a high-interest savings account.

AND that balance was not included in the earlier calculation of our timeline to financial independence.

The intent of that cash was to help us reach FI. You may recall that we considered two scenarios: 1) Invest that cash in the stock market OR 2) Purchase a Rental Property. Here’s a look at those calculations from two years ago.

Investing in the stock market would shorten our then-timeline of 8 years to 7 years, allowing us to reach financial independence in 2027. Buying a rental property, would instead shorten our timeline to ~6 years, or reaching financial independence in 2026.

Scenario 1: Investing the Cash in the Market

Scenario 2: Investing the Cash in Real Estate

These two scenarios were also in the context of the other big lifestyle change that we felt looming: Jess quitting her part-time job and trying out full-time entrepreneurship.

Two years ago, we didn’t know when we would pull the trigger and we expected our income to decrease in the short term. We ended up making the decision for her to quit her day job less than a year later. As I already mentioned, her quitting her job actually increased her income.

There’s always more clarity looking back. But the concerns around maintaining (or increasing) income were there – as was the courage to take the leap. At the time, we thought that fully embracing Slow FI and designing our lives would extend our timeline to FI to 13 years (when we would be 46).

We now have the benefit of 2 MORE years of data (4 years after our first plan). Let’s take a look at where we are now and the grand plans that we are creating.

Our Current Financial Independence Plan

Our Current Numbers

- Age: We will soon be 35 years old.

- Assets: We have 10-11x our annual living expenses currently invested in the stock market, excluding equity in our home and additional cash reserves.

- Savings Rate: This year we are expecting to save 60-65% of our take-home pay, when excluding big purchases planned this year. It will be more like 40-45% when including these major expenses.

- FI %: We are able to cover approximately 35-45% of our annual expenses indefinitely by using the dividends and appreciation from and without depleting our assets (using a 3.5-4% safe withdrawal rate).

We’ve made some significant progress in the past ~2 years. We continue to chip away at our wealth accumulation goals.

Based on our savings rate, assets, and a few other assumptions about market performance, we estimate that we would reach financial independence in 5.5 – 7 years. This also assumes that we keep everything the same for that time frame.

Which we know is not going to be the case – but more on that later.

Our steady progress is great. But, what is most remarkable is that we have continued to prioritize designing our ideal life while making progress towards our financial goals.

This includes spending more money on health, hobbies, friends, and a few other categories. We could have made even more progress – but we are happy with the trade-offs we have made. And we are still saving a high % of our income and accumulating wealth.

Our Financial Independence Strategy Moving Forward

Our plan to reach financial independence has shifted significantly over the past 4 years. We were originally on an 11-year path to reach FI, and now a lot has changed. Jess shifted to work part-time and then quit that job to go full-time entrepreneurship.

Things have gone so well with entrepreneurship that we are planning yet another change.

We are planning for me to quit my day job and switch to working on the business. We’re still figuring out the right timeline, but right now the thought is that I will likely transition out of my day job in the next two years.

While I enjoy my job, it does take a lot out of me – and doesn’t offer me the flexibility that I would like in order to travel more and pursue other interests.

To help with determining when to make the change, we’ve modeled out a few scenarios.

There are a lot of unknowns when it comes to looking to the future. We can’t know for certain the timing of each lifestyle change and income level at each step in this scenario. But that doesn’t stop us from using scenarios to understand the possible implications. We have modeled out what this could do to our path to financial independence.

The most likely scenario that we are considering is for me to leave my job mid-next year. This means we’d have another 1.5 years of our current income and savings rate, and then an assumed huge drop in both metrics.

With conservative assumptions around revenue for our business, our timeline to FI could extend to 10 years. Even with saving a small amount each year starting in 1.5 years from now, we would still reach financial independence by the time we are 45 years old.

This scenario assumes our savings would decrease significantly. Most of the progress toward FI would be due to appreciation of our investments. Because we have saved so aggressively to this point, we have the luxury to scale back and still achieve FI.

This is a nice reminder of how financial freedom is incremental. Even though we are years from achieving FI, we can leverage the financial freedom that we do have to optimize our life.

We are setting some milestones that we would like to achieve before we make this change (more on those in a future post). But, we should be able to achieve a location-independent lifestyle sometime in the next two years.

I’m going to let that sink in for a minute. That’s the first time that I’ve typed that out.

When we started this journey 4 years ago, I never would have imagined that we’d be where we are today. That’s the beauty of the journey.

There are twists and turns along the way. An adventure almost requires that to be the case.

Most people pursuing FI wouldn’t consider slowing down. But our mantra is to enjoy the journey to financial independence. We’re happy to extend our journey if it means we have more freedom earlier.

Why wait another 5-7 years to do what we want, when we can make incremental shifts to achieve that sooner.

This is why we think financial independence is both a journey and a destination. Figuring our ideal lifestyle is our frontier – both the journey of optimizing parts of our lives while buying our freedom.

And that continues to be exciting and motivating all at the same time. It is the near-term milestones along the way that keep us motivated and help us discover and design our ideal life.

While we may have a better sense of what will make us happy than we did years ago, there’s still a lot to figure out. We’re going to do a lot of experimenting and testing lifestyles to see what works for us. We will continue to share both our financial and lifestyle design progress with you along the way.

Isn’t it cool that you are able to think about FI as a reality and have retiring in your early 40s as a possibility? Especially since most people never heard of the concept of FI or RE until just a few years ago. Congrats!

Hi Nathan,

Yes, it is really cool! I am still really amazed sometimes that this is a real possibility. I wish more people knew it existed (i.e. part of why we created this blog!)!

Thanks,

Jessica

I am 39 years old and also working towards FI. I’ve been saving for retirement for many years but now want to accelerate that a bit. It’s definitely a challenge to cut back and live off less. For instance, I am paying a lot for a rental right now because I have a big lab and I’d rather have a yard for him to play in. I’ve cut back significantly in other areas like travel. My budget is the same. I just spend it differently.

Hi Stacy,

Thanks for your comment! When I read this, I thought of something – there are two levels to pull to increase your savings rate. One is to cut back and live off less. The other is to make more money. Have you considered focusing on the latter if you don’t feel like you can cut back on your spending?

On the other hand, I also feel like it’s important for us to live happy and fulfilling lives along the journey, so cutting things that bring you joy (a large yard for your dog) just to retire earlier, probably wouldn’t make sense. I think the most important think is to be intentional about how we spend our money and if it’s adding value to our lives.

Thanks again for the comment,

Jessica

The biggest issues with FI right now are kids and health insurance. Both make it difficult to survive longer term without at least one parent having a job. I think that even if we were able to generate the income necessary, one of us would need to work part time for the health insurance part…the costs are rising much faster than inflation, and eventually will take a major chunk out of living expenses.

Hey Late Start FI,

Thanks for commenting. Yes, health insurance is definitely a barrier (hopefully not insurmountable), and thing could get better in the coming years. We will have to wait and see. Many part-time jobs don’t provide benefits though, unless you work over 30 hours.

Thanks,

Jessica

Enjoyed this! I love seeing other people also taking the time out to really think about what works best for them and not just accepting the standard path.

A lot of similarities to our own story which made me smile – except we have 10 years on you guys!!

I like you’re looking at building up your online business. We accidentally fell into S working online and even though we planned for us both to quit 2 years, he’s carried on since it works so well with slow travel. We now call ourselves “part-time nomads” !!!

But you are right, there are so many ways to FIRE and you need to do what works best for you guys – not for anyone else and not just what’s fastest. There’s way more to life than money. Good to see you making great progress!!

Hi Michelle,

Thank you so much for the comment. I love hearing encouragement from people who are a little further along in their journey. I’m looking forward to working on your Slow FI interview soon. 🙂

Best,

Jessica

Totally agree. Life is all about striking the right balance. This especially holds true while on the path to FIRE.

Thank you for the comment!

This is wonderful to see a well thought-out plan and strategy to attack FI and then also seeing the flexibility to be able to change the plan as you’ve got more new information.

Glad to also hear the entrepreneurship part is going well – and who knows, when you switch from your more draining full time job to doing your own thing, the entrepreneurship results might even skyrocket due to more time being invested into it.

Hi Angie,

This is so true! I definitely think this could be possible, but we also want to prepare for it not to skyrocket (we’re find if it can just cover our costs). 🙂

Jess