For the last few years, Corey and I would sit down together at the end of each year to do “annual financial planning.”

For the last few years, Corey and I would sit down together at the end of each year to do “annual financial planning.”

Corey would want to save a higher percentage of our income and mention the possibility of retiring early. I would roll my eyes, say I wanted to live my life now, and then we’d compromise and move on.

I had virtually no understanding of the mechanics of personal finance. When Corey asked me to read Your Money or Your Life in a book swap, I begrudgingly agreed (and only because he was reading a book I recommended about women in the workplace).

Because I wasn’t excited to read the book, I was skeptical at first. However, once I had read a few chapters, I was hooked.

The book wasn’t just about money or a single aspect of money. It did not assume that your “financial life functions separately from the rest of your life.”

In the introduction to the book, Vicki Robin and Joe Dominguez ask:

My answer to that question was a resounding NO.

The book illuminated where my own views on work and money had become distorted.

This shined a light into a dark place in my life that I didn’t want to explore because I didn’t believe anything could be done to change it.

The majority of my time was spent at work, preparing for work, commuting to work, stressing about work, and trying to unwind from work. I was chasing promotions and battling depression.

I knew that I couldn’t continue my life this way for much longer. The problem was I had no idea what I wanted to be doing with my life. I just knew that what I was doing wasn’t it.

Reading Your Money or Your Life was like a breath of fresh air for me. It helped me to see that a different roadmap through life was actually possible. This new map allows you “to choose your own path through the territory of earning and spending – and to integrate that path with the rest of your life.”

This was a big promise, and the authors did not disappoint.

Major Themes of Your Money or Your Life

The book as chock full of helpful insights about both the philosophy and the mechanics of money and financial independence. While I can’t share them all, there were a number of insights that served as a launching point, or should I say basecamp, for our Fioneering journey.

Envision Your Ideal Life

The authors suggest that in order to bring your life into alignment you need to envision what your ideal life would actually look like.

A simple question kicked everything off for me.

When I first read it, I had no idea how to answer the question. I had accepted that working full-time for 40 years was what everyone did, even if I wasn’t happy with it. I hadn’t realized that there were other options.

Because I couldn’t come up with anything right away, I put it on my list of things to reflect on. At the time, I had a mental block.

I didn’t allow myself to think about the question because I didn’t think it was worth thinking about. If I did think about what I wanted, it would be too painful and disappointing when it was impossible to achieve.

It honestly wasn’t until I understood the mechanics and knew that financial independence was actually possible that my mind opened, and I was able to consider the possibilities.

The Mechanics of Financial Independence

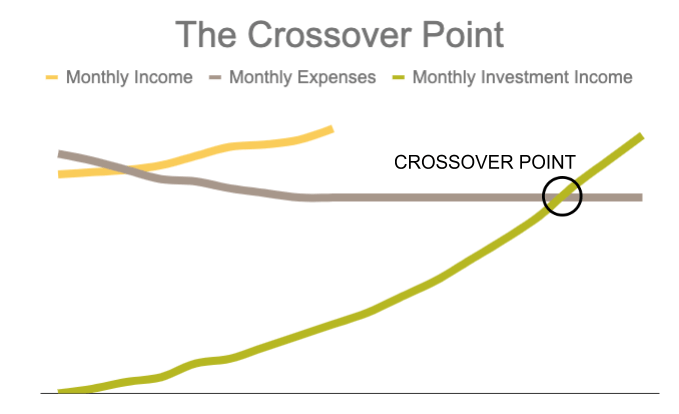

While the mechanics of financial independence now seem quite simple to me, at the time, it felt mind-blowing. In the book, the authors recommend creating a chart where you map three things:

- Your Income

- Your Expenses

- Your Investments

Then you’d do 2 things:

- Grow the gap between your income and expenses by increasing your income and/or decreasing your expenses.

- Invest the savings, so that your money would earn more money

Once you reach the “Crossover point,” where your investments could cover your expenses, you’d be financially independent.

Understanding this simple concept was an epiphany for me.

Of course, Corey already knew this and had been tracking our income, expenses, and investments already.

When I turned to him and asked, “Is this real? Is this actually possible?”, he was able to pull up a spreadsheet and say, “Yes, and we’re on track to be financially independent in about 10-12 years.”

While we don’t track our finances on a wall chart the way the book recommends, we do track our income, expenses, and investments on a monthly basis using Personal Capital.

This tool has a helpful dashboard where we can see every transaction in one place. We can see our income, our expenses, our cash flow (the gap), and our investments and their growth over time. This allows us to track our progress just as well as a wall chart would.

Spend money consciously

While extremely helpful, the act of tracking spending doesn’t automatically translate to spending less. You need to actually change your spending habits. This book was a proponent of mindful spending.

Prior to reading the book, I didn’t have a framework to think about spending money beyond spending less than I earned. To be honest, that wasn’t very difficult to do.

I’ve always lived within my means, and we were gaining more experience in our careers and getting fairly hefty raises year after year.

We were starting to see some pretty dramatic lifestyle inflation around our food and entertainment spending.

I didn’t really think about money on a day-to-day basis, but this book changed everything.

Money is Time

In the book, the authors focus a whole chapter on “life energy,” which basically means the precious and limited time we have on this earth.

At the time, this was a completely new concept for me. When we buy stuff, we ultimately pay for it with our time.

This led me to calculate what they call the “True Hourly Wage.”

This made me think about my job in a much different way. Even though I was getting paid a fairly good salary, it was very illuminating to subtract costs like gas and business attire from the earnings. It was even more illuminating when I included both commute time and the extra hours worked in my total weekly job-related hours.

I realized that while I made a pretty good salary, my true hourly rate was quite low because of both the additional costs and additional hours. In fact, my true hourly rate is actually quite a bit higher in my part-time job because of a shorter commute and fewer extra hours. While I make less, each hour of my time is worth more.

Once you actually calculate your true hourly rate, you can see two things more clearly.

- If you are getting paid enough for your life energy (and if not, you can get a higher paying job or a job with fewer hours).

- How much of your life energy you are using to pay for things that may or may not bring fulfillment.

Reflect on Your Spending

Once you realize that you are trading time for money, the book instructs you to look at your spending to see what you are spending your precious money (and therefore your time/life energy) on.

There is one question the book recommends asking during this reflection that has really stuck with me:

I could also phrase this in an easier way – Was it worth it?

When we went on vacation last summer, we spent time together reflecting on our spending (with the help of screenshots from Personal Capital because we didn’t have internet). We discussed this exact question – Was it worth it? Did we receive fulfillment, satisfaction, and value in proportion to the life energy spent?

As we analyzed our spending, we realized that there were many areas in our lives where it was not worth it. We were not receiving the requisite fulfillment, satisfaction, or value in many areas.

1. Food

We realized we spent an inordinate amount of money on groceries and eating out. We’d also increase these costs by ordering in fairly often. When we ordered in, other groceries would then go to waste.

We realized that we were not getting fulfillment or satisfaction from it. I was so sick of ordering in that when we proposed it as an option, I often couldn’t actually think of any food that I would want to eat.

We decided that we needed to drastically overhaul our meal planning and food spending.

2. Travel

We did decide that travel was important to us. We receive fulfillment, satisfaction, and value from exploring new places and learning about new languages and cultures. We actually decided that we wanted to travel more and realized that we could travel more for less through travel hacking.

3. Miscellaneous Purchases

We also became much more mindful of the random everyday things we spent money on.

We got no more value out of a book we bought than one we borrowed from the library. We stopped buying books off Amazon, and I canceled my audible subscription.

We also started being more intentional about the money we spent with our friends. We realized that we actually got less fulfillment and satisfaction from a fancy dinner out at a restaurant than when we invited friends to come over for a meal. Therefore, we started inviting our friends over more often and to do free or cheap activities.

Institute a Regular Reflection on Spending Habits

Without a regular reflection, it’s easy to fall back into old habits. For example, earlier this year when I looked at our restaurant spending, I realized that it was quite high again. Because I had just started my new job, everyone had been asking me to go out for a get-to-know-you lunch or coffee. On top of that, colleagues from my previous job wanted to reconnect over dinner, coffee, or drinks.

My food spending was getting out of hand…again.

Through a review of our spending, I was able to reflect on how this spending was not bringing me fulfillment or satisfaction in proportion to the amount of life energy it cost. I could bring my lunch and still have lunch with coworkers. We could take a walk instead of going out for coffee. I could propose cheaper alternatives to a meal out when someone wanted to get together.

Through this mindful reflection, we got our restaurant spending back down to a good level for April.

Even with the blip in our restaurant spending earlier this year, we now spend quite a bit less money than we used to. It’s not because we are penny-pinching or have a super strict budget. It’s because our whole perspective on money has shifted and we are much more mindful of each purchase.

Now that I realize that I “buy” money with my time, it is a precious resource that is not to be wasted. I regularly think about whether I’m getting fulfillment, satisfaction, and value from anything I would purchase. If not, then the money would be better used to buy back my future time.

The best way for me to spend less money is by being more intentional.

The Beginning of a Journey

Reading this book was the beginning of my Fioneering journey, and my life has completely changed since reading it.

Before reading the book, I worked 50 hours/week and commuted 2 hours/day. My life was consumed by work. I was trying to get meaning and purpose out of succeeding in my career, and it just wasn’t happening. I was constantly frazzled, stressed, and depressed.

Now, I work part-time (24 hours/week), and my commute on my work days is less than 1 hour/day. Now I have a much richer life.

I have life goals instead of only having career goals. I have discovered many additional ways that I love to spend my time. I feel much more balanced. I now even have days when I feel like I have an excess of mental energy, and I get to decide how I want to use it.

Reading this book led me to make significant life changes:

- It guided me through the process of envisioning my ideal life.

- It helped me understand the basic mechanics of financial independence.

- I have become much more intentional about the way that I spend money because I understand the link between money and time.

Now when I ask myself the same question from the beginning of the book, “Is your life whole? Do all of the pieces – your job, your expenditures, your relationships, your values – fit together?”, my answer is very different.

I can say YES. While there is always room for improvement and better alignment with my ideal life, my life is whole and it all fits together.

I now know that I don’t need to make a choice between my money and my life; I can engineer my life to have both.

Awesome stuff. So many have referred to this book as almost a bible of FI that as someone who is blogging and living FIRE, I am ashamed to have only read parts of it. I like the crossover point concept for motivating one to get to FI. Also, wow I am just finding your blog and checked out your bucket list post too. I also have a bucket list and share many of your same philosophies on the value and pitfalls of such a list. Excited to read more Jessica

Thank you so much for your comment! I definitely recommend the book (obviously). 🙂 Also, I checked out your bucket list! I see that you are interested in learning to sail.

Two summers ago we learned how to sail. We joined a community boating club and took lessons for the summer. We were out on the water almost every weekend for a couple of months. It was great. It’s possibly something to get back into – but it’s an expensive hobby and we found ourselves too busy the last couple of years to pay for a membership.

I also just followed you on Twitter so I can engage with more of your content. Thanks again!

Jessica

Great review. This was one of the first books I read early in my financial journey. It completely changed my mindset on money. This is a timeless book that everyone should read!

Thanks for reading! It is such a transformational book; I agree that everyone should read it!

Best,

Jessica