My first introduction to Financial Independence was reading Your Money or Your Life.

The next place I turned to learn more about financial independence was the Choose FI podcast. I listened to my first episodes on the way to our famed Maine trip in 2018. While in Maine, we officially decided to pursue financial independence.

On the four-hour drive to Maine, we listened to 3 episodes, and I couldn’t get enough. We listened to:

- Episode 4 – Get Off the Hamster Wheel – This episode goes into Jonathan’s backstory.

- Episode 21 – The Pillars of FI – This episode goes through all the basic tenets of FI. It touches on index fund investing, savings rate, spending on housing, transportation, and food, travel rewards, and increasing your income.

- Episode 7 – Crush your Grocery Bill – As you might know, food spending has been our biggest challenge so far. This episode opened my eyes to the possibilities of how to reduce food expenses.

The podcast helped me understand that pursuing financial independence was actually possible. Real people were doing it, and I was ready to dive in headfirst.

When I learned that there would be a Choose FI book coming out this fall, I reached out to get an advanced copy.

The book hits stores on October 1st, 2019, so you can buy it then. You can also pre-order it now or recommend that your library get the book.

Meeting the Author, Chris Mamula

I recently had the opportunity to meet Chris Mamula, the author of the book. We were both attending FinCon, a financial media conference. Chris also writes for Can I Retire Yet?

We had a riveting discussion about the Choose FI book. In the discussion, I highlighted both the things I enjoyed and critiques I had. I’m generally a pretty honest person, sometimes too honest. After our initial conversation, I worried that I gave Chris the impression that I didn’t enjoy the book.

I found him at the conference the next day to reconnect. He actually told me that he truly appreciated the honest dialogue about the book. Most people only tell him positive things, and he was hungry to have an open dialogue about what could have been better.

He also shared with me some of the things he’s wished he’d been able to do differently with the book. It felt like the start of a burgeoning friendship.

Chris recently even (satirically) offered to write my memoir. Here’s the proof:

I’m ready to write my next book. . . just waiting for the right offer. pic.twitter.com/wTpJI36DBs

— Chris Mamula (@caniretire_yet) September 18, 2019

Now that you know that Chris is an awesome person, let’s talk about his book!

Impressions of the Choose FI Book

I read devoured the book in a 3-day weekend while we were camping earlier this summer. It helped that we were disconnected from wifi with no distractions. It’s unusual for me to finish a book in 3 days. This should tell you something about the quality of it.

Ideal Audience of the Choose FI Book

This book can best be described as a “how-to guide.” If someone already knows about financial independence but still doesn’t believe it’s realistic, this book is for them.

I would have loved to read this book immediately after reading Your Money or Your Life. Your Money or Your Life left me inspired, but I didn’t know what action to take next. I also didn’t fully believe that financial independence was possible until I understood the mechanics.

The Goal of the Book

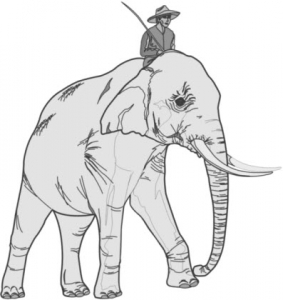

Reading the Choose FI book reminded me of a motivation framework that I’ve introduced in previous posts. This framework from the book Switch uses the analogy of an elephant and a rider.

The elephant is your emotional mind and needs to be inspired to take action. Without inspiration, it’s unlikely to move in the direction you’d like it to go. The rider is your logical mind that knows the steps and can point to the destination.

Without both having motivation and knowing the steps, your elephant wouldn’t know where to go next or what to do. This book demonstrates that financial independence is possible. It also gives you actionable tips to make progress in your own life.

This book is not void of motivation (see one of my favorite quotes below). The core purpose is to inform and help the audience believe that FI is possible.

“FI is not about retiring early or retiring at all really. It’s all about having the freedom and flexibility to design your life in alignment with your values. You can work on things important to you. You can work at your own pace. Or you can choose to not work at all. FI gives you the power to decide.”

Strengths of the Choose FI Book: Simplicity and Potentiality

I thoroughly enjoyed this book. Chris pulls out the core concepts of financial independence that were featured in the podcast. He then organizes them into a coherent narrative.

Financial concepts often feel opaque and complicated. This book was clear and easy to digest. It will help people both understand financial independence and believe that it could actually be a reality in their lives.

Communicating the Big Picture

The book outlines the basics of financial independence well: 1) Spend less, 2) Earn more, and 3) Invest Better. It lives up to its subtitle: “a blueprint for achieving financial independence.”

The Choose FI book explains the important big-picture concepts flawlessly. Chris shares the importance of increasing your savings rate, understanding opportunity costs, and aggregating marginal gains.

This concept of aggregating marginal gains is one that was new for me from the Choose FI podcast. Chris articulated it well in the book.

“The concept of aggregating small wins is powerful. Choosing FI is not a single choice. It’s many small choices that continue to build on one another until you eventually reach a tipping point.”

Introducing the Tactics

As important as it is to understand the big picture, it’s even more important to understand the tactics. What changes can we make in our lives that make financial independence a possibility?

The book includes practical ideas for increasing your income and reducing your expenses.

To increase your income, the book recommends hacking college and increasing your income in your day job. Then, you can put your money to work for you in investments.

You can increase your income by building your skills, networking, or switching jobs. You can invest your hard-earned cash in the stock market, real estate, or by building your own business.

To decrease expenses, the book focuses on the big three expenses: housing, transportation, and food. These three expenses make up the vast majority of our budgets. If we can get these right, we’ll be in a much better position.

The Choose FI approach also emphasizes aggregating marginal gains. The book highlights small recurring expenses, such as cell phones, cable, and insurance. While these costs might be small, these are all marginal gains that can make a big difference in the long-run.

You might not think these small everyday decisions make a big difference. We’ve proven otherwise. We reduced our expenses by $17,000 in our first year of pursuing financial independence.

We didn’t do this by moving to a low cost of living area or selling our cars. We did this by aggregating the marginal gains. One thing might not make a big difference. If you put all the “one things” together, it does.

We attribute this dramatic change in spending to a variety of things. Utilizing travel rewards allowed us to save money on vacation. Going out to eat less and buying in bulk allowed us to reduce our food spending. We also spent less on general merchandise (i.e. random stuff).

Aggregating the small wins works! Thank you, Choose FI for teaching me that!

Critiques: The Choose FI Book Doesn’t Challenge the Traditional FIRE Narrative Enough

I mentioned this critique when I spoke with Chris a few weeks ago. Chris was surprised at first.

The Choose FI book does challenge the traditional early retirement narrative in some ways. It’s definitely not about retiring early so you can sip piña coladas at the beach.

“Early Retirement is very different from traditional retirement. It’s not about what you are running from, but what you are running to. It’s not about never working again but claiming autonomy, mastery, and purpose for your life. You get to pick and choose the activities that light you up and design a future you can get excited about without the risk or fear of how you’ll keep the lights on or feed your family.”

The book articulates the purpose of financial independence as figuring out what you want to do in life and, then, making it happen. While I agree, I’d like the FI community to start thinking more expansively about financial freedom.

Focusing on Early Retirement is Incomplete

People who are financially independent can focus on flexibility and building a life that you want. Claiming autonomy, mastery, and purpose in life is inspiring. Picking and choosing the activities that light me up is what I want to be doing.

As a Slow FI Enthusiast, my main critique is that I don’t need to wait until early retirement to start changing my life. Yes, there is a bit more risk. Once you have a large enough emergency fund and investments, you can work toward a “future you can get excited about” now with minimal risk. You don’t need to wait until you reach FI.

I can achieve incremental financial freedom along the journey. This inspires me more than early retirement.

The Financial Independence Milestones Focus on Your Early Retirement Number

As some of you may know, I don’t love the traditional FI milestones. The reason why is that most of these milestones are focused on your “FI number.” This is the amount of money that you need to be financially independent and/or retire early.

I appreciate that the book affirms that financial independence is not all or nothing. Chris focuses on the power of F-You Money and how it can shift the power dynamic that you have with your employer. I love this!

I don’t think that the book (or the podcast) has taken this idea of incremental financial freedom far enough in the milestones. The milestones they articulate are:

- Getting to Zero – You have more assets than liabilities

- Fully Funded Emergency Fund – 3-to-6 months of living expenses

- Hitting Six Figures – Once your investments hit six figures, this cushion allows you to start using F-You Money

- Half FI – 50% of your FIRE number

- Flex FI – Sustainable passive income can cover all your essential expenses

- Lean FIRE – 80% of your FI number

- Financial Independence – 100% of your FI number, or 25x your annual expenses

- Fat FIRE – 120% of your FI number

Many of these milestones reinforce that the goal is to reach a specific number. For me, reaching my “FI number” is not my main goal. My main goal is to balance planning for the future with happiness along the way.

These milestones have little meaning for me today. If I know that I’m between six figures of investments and half FI, what does this mean for my life?

Because of this, I decided to create my own FI milestones earlier this year. These new milestones focus on how much active income that I would still need to generate.

If I knew that I only needed to generate $30,000/year of active income, it could free me up to work fewer hours or to do something I’d enjoy even more.

The Choose FI Book Overemphasizes Finding a High-Paying Job

I am a proponent of getting paid a fair wage for the work that you do and increasing your income. At the same time, choosing a career path is about more than earning a high income.

Your career is an opportunity to find out what works for you. It’s an opportunity to explore what could be a good fit for your experience, skills, and personality.

The chapter about increasing your income in your day job focuses on pay over passion.

“A common pattern among those who achieve FI quickly is to choose a career that commands an above-average income. It’s popular to say you should “follow your passion.” Others might say, “find a job you love, and you’ll never work a day in your life.” Those make great bumper stickers, but they don’t typically work well in the real world. Maybe a better idea is to find a career that interests you and allows you to earn a solid income. Then learn to love it, or at least like it, while saving a high percentage of your income, allowing you to achieve FI quickly.”

I agree with most of this in theory. Of course I want a career with an above-average income. I also don’t believe that you should necessarily feel passionate about your day job.

This still feels incomplete though.

Had I followed these principles during college and early in my career, I would not be the person I am today. Because I embraced a process of exploration, I learned a lot about myself.

For example, I took an anthropology class in college (not a big money-making career). I realized that I loved learning about cultures and languages. I ultimately chose this to be my major area of study.

While in high school and college, I volunteered a lot. Because of this experience, I decided to pursue a job working in a nonprofit organization. I wanted my career to make a difference in the world. I made this decision knowing that nonprofits typically pay lower wages than corporations.

I wasn’t paid well right away. I took a job through AmeriCorps with an $11,000/year salary while living in the NYC Metro area.

This was an extremely valuable experience. It enabled me to break into a field that I was very interested in when I was hired on full-time to the organization after my fellowship.

My career started out in fundraising and partnership management. I later switched to training and supporting the people who did that work. From this experience, I realized that I enjoyed training and coaching.

This led me to transition into human resources, where I got to focus on professional development and organizational culture (my “worthless” anthropology degree actually helps me out a ton with this!).

From these experiences, I discovered what I am passionate about. I want to help people learn things that I’ve learned (often the hard way) throughout my life. This is why I started this blog and why I am considering doing career and/or life coaching.

If I had focused my career on earning a high income, I would likely not have learned these important things about myself. I wouldn’t have the same confidence in the goals that I have for my present and future.

I don’t want you to miss out on the experiences and exploration that can illuminate who you are and what you want. If you can still pay your expenses, it might be worth getting paid less to gain valuable learning experiences.

One important thing to note is that it’s not necessarily an either/or. There are many people who have chosen to take a pay cut to do a job that is a better fit for them. Within a few years, they often make more money than before. When you enjoy your job, you are often better at it.

Even though I took an unconventional path, I still worked my way up to making a good salary in a leadership role. Earlier this year, I was able to take a pay cut to work three days/week. With this shift, I am still paid a solid middle-class salary.

I’ve learned that making a high-income isn’t everything. I now make less money and have a job I enjoy. It’s no surprise that I have less urgency to retire early. While I do want to reach FI by the age of 50, I’m not in any particular hurry.

I would have loved to see lifestyle design feature more prominently in the book.

More Diverse Representation Would Make the Book Even Better

When I had the opportunity to meet Chris, he shared that he would have liked to feature more diverse voices in the book. I appreciated this transparency. He also shared with me a reflection that he wrote on his own blog.

“The downside is that a book is finite, while the podcast can continue on. In order to compile the podcast interviews into a manageable manuscript, we had drawn an arbitrary cut off line for the interviews included in the book… Because of this, some of the best stories told on the ChooseFI podcast didn’t make the book.”

Because Chris began the book in late 2017, he was only able to include interviews from the beginning of the podcast.

I would have liked to see more stories from women and people of color featured in the book. The challenge is that there were fewer women or people of color on the early days of the podcast.

In the last couple of years, the FI community has begun to recognize more diverse voices. The Choose FI podcast has more recently interviewed more women and people of color. Unfortunately, many of these interviews were recorded after the manuscript was complete.

This makes me wonder what the representation in the book would look like if it was written 5 years from now. I’m interested to see the FI community continue to evolve.

My Key Takeaways from the Choose FI Book

This book is an incredible resource for someone who is toward the beginning of their journey to FI. If you already know about financial independence and want to learn how to make it a reality, pick up this book.

This book communicates the mechanics of FI in a clear and compelling manner.

Even though I have some differences in opinion with this book (and the traditional FIRE narrative), it gave me a platform to reflect on my own path.

The idea of marginal gains and making small changes finally stuck with me in a way it hadn’t before.

The book made me reflect on the role of work in our lives. I was also motivated to understand how to use the idea of marginal gains in more areas of my life. I want to make “marginal gains” not only to reduce my spending. Small shifts to improve our lives can allow us to be happier and enjoy the journey to financial independence.

Thank you so much for your review! Glad you clarified that it is not out until October as I kept texting my husband to see if my copy had arrived (out of town now). I so agree with you when it comes to the FI number thing. That has n we resonated with me nor did the milestones associated with it. I also like designing my life today in a way that makes me not crave retirement. I found the podcast this past April and have been catching up since and love how the latest episodes have more women and diversity in general 🙂

Fantastic book review, Jessica. I appreciate your critiques as well, and that Chris was able to speak to some of them. I’ve heard nothing but great things about the book, but I won’t be able to make up my own mind until I get it for myself.

Keep up the great work designing your life on the way to FI.

Great insights on the book! It’s true that the Choose FI book is missing some important aspects like Slow FI. Of course no book can cover every possible angle, but I agree that there could be more diverse paths of FI explored in the book. Maybe a book on Slow FI will be your own big project one of these days!

Hi Kate,

You are so right. No book can include everything! I’d love to write a book someday on Slow FI and Lifestyle Design. We will see!

Thanks,

Jessica