We just made a huge purchase. In fact, it’s the second-largest purchase we’ve ever made (after our condo).

We just spent approximately $60,000 on a NEW Mercedes Sprinter Van. Yup… that’s a LOT of money.

After we receive it in December, we’re planning to hire someone to help us convert it into a campervan. That will also cost a pretty penny.

In this campervan, we will have:

- A queen-sized (ish) bed

- A dedicated bathroom with a shower and toilet

- A kitchen including a sink, stove burners, a microwave, a dorm-sized refrigerator, food storage, and counter space

- A small seating area that will include two seats and a table (which can be converted into a bench/couch)

- And more…

The materials alone to convert a cargo van into a tiny home on wheels will cost about $35,000. And, that’s before we pay for any labor.

Oof, this is going to be a lot of money.

Three years ago, I can’t imagine I’d ever have felt comfortable doing this. I could barely bring myself to buy Smartwool socks. Instead, I chose to stick with the cheap pack of socks from Costco that I needed to replace every year.

I used to make every financial decision asking myself these questions:

- Do I actually need that?

- Could I find something cheaper?

- Do I want this more than financial freedom earlier?

Of course, I also hated my job, so I couldn’t think of anything I wanted more than financial freedom.

It’s amazing to see the progress I’ve made over the last 3 years. Somehow, I’ve gotten comfortable with spending $100K+ on a campervan conversion because of the value it will add to our lives.

How We Got Comfortable Making Such a Huge Purchase

You might be wondering, “What changed? How did you go from being a Costco sock-buyer to someone who could spend so much money on something that’s truly a want (not a need)?”

There are three main things that helped us get to a level of comfort to be able to do this.

- I needed to feel like I deserved a joyful and fulfilling life.

- I discovered exactly what I value most and what my ideal lifestyle looks like.

- I gained total clarity about my financial situation.

These helped me to:

- Realize that I could use the financial freedom I’ve built to improve my life.

- Be decisive because I knew the decision would align with my values.

- Understand both the short- and long-term impacts of a decision.

- Make trade-offs between life satisfaction and our FI timeline with eyes wide open.

I know that’s a lot. The rest of this post will break down the things we’ve learned into actionable insights that you can actually use.

What to Do Before Making a Huge Purchase

If you want to get more comfortable both emotionally and financially before making a big purchase, there are 5 main things to do.

- Decide you deserve it

- Articulate what you value

- Assess how the decision will impact your long-term financial situation

- Decide whether the trade-off is worth it

- Determine the short-term logistics and financial impacts

1. Decide You Deserve It

So many people (including me) have such messed-up views about what they deserve. I grew up in a super religious context where self-sacrifice was praised. I always assumed I would (and wanted to) be poor. You were a better person if you suffered. You were more virtuous if you didn’t have money.

I don’t need to go into too much detail here (you can read a full post I wrote about this). Suffice it to say I didn’t feel like I deserved to be happy. There were so many people in the world who were suffering. Why should things be any better for me?

Well, we all know where this mindset got me. In my previous non-profit career, I worked way too much. I gave too much of myself. I’d come home from work every day and crash. I’d put just enough back into the “gas tank” (i.e. my energy reserves) to make it through the next day. To go with a sports metaphor, I left it all on the field. Every single day.

Then, things fell apart.

I started experiencing severe anxiety and panic attacks. I was so burned out that I needed to take 6 months off of work just to be able to function again. When I went back to work, I took a part-time job that was well below my skill level, simply because that was all my mental health could manage.

The biggest, most important thing that I learned was that I deserve to be happy. We all do. Happiness and joy are not finite resources. My joy doesn’t take away joy from someone else.

I don’t have to suffer simply because other people are suffering. In fact, I can make the most impact on the world around me when I’ve filled myself up. When the joy I experience can overflow to the people around me, that’s when I’ll be able to make the most impact.

This is why the first step to making a big purchase (or making any other decision) that will improve your life is to decide that you deserve it. Without that mindset, you may never feel comfortable making such a big decision.

2. Articulate What You Value

When you know what you value most, you can make decisions that align with those values.

One activity that helped me define my values was working through a book called the Desire Map. The main idea is that if you can decide how you want to feel, then you can design your life to allow you to feel this way more often. They can also give you an indication of what you value most.

After working through this process, I came up with a list of 5 core desired feelings. I wanted to feel:

- Energized

- Adventurous

- Creative

- Balanced

- Authentic

For me, this was an indication of what I value most:

- The freedom to structure my work and daily life in a way that gives me energy (rather than drains me).

- Travel, exploration, and trying new things.

- Creating things that help others (and as a way to express myself). Right now, this looks like blog content, workshops, courses, etc.

- Wellness and well-being (physical, mental, and emotional).

- Strong, reciprocal relationships where I can be authentic and open.

When thinking through the decision to purchase the campervan, we realized that it reflected our values in so many ways.

- It would allow us to travel around the country (or continent), explore new places, and try new things. It would enable so many adventures.

- Getting out into nature and being physically active supports our well-being.

- Given the anxiety and mobility issues that I experience, traveling in a van is an awesome way to travel. It allows us to take breaks wherever we are and to slowly create plans about what we want to do next.

- We will be able to work from our van, so we don’t necessarily have to take time completely off from work while traveling.

- It’ll allow us to enhance our relationship, and it will allow us to visit our friends who live all across the country.

Besides our stated core values, it supports our quest to be more eco-conscious and mindful of our consumption. When you are traveling in a van, you are ultra-conscious about how much electricity and water you are using. It’s very apparent that these are not unlimited resources.

It also supports my desire to be more minimalist. I’ve done so much decluttering over the last couple of years (and still have a lot more to do). Many people say that when you spend time traveling (or living) in a van, you become very aware of what you actually need and truly value.

Suffice it to say, this purchase will add so much value to our lives.

To make purchases that align with your values, you must know what is uniquely important to you. What makes you feel most alive? What matters to you most?

To identify your own values, I’d recommend two activities:

- Work through the Desire Map to understand your core desired feelings.

- Work through this post I wrote on Identifying the Core Elements of Your Ideal Life

3. Assess How the Decision will Impact your Long-Term Financial Situation

The first question you’ll likely ask yourself is, “Can we afford it?”

It’s important to define what I mean by “afford it.” I don’t simply mean that I have the money or the ability to get the money right now.

What I mean by “afford” is:

- Either having the money on hand OR the cash flow needed to finance the loan (while still comfortably covering my everyday expenses), AND

- That spending the money will not jeopardize our traditional retirement (at the age we choose)

This is why it’s important to know your numbers! These are some of the key numbers you need to know:

- Your income

- Your expenses

- Your current savings rate

- The balance of your investments

- The balance of your emergency fund (and/or F-you money)

- The timeline at which you’d reach FI at your current savings rate

When you know these numbers, you can assess how much a big purchase will impact your long-term financial situation.

To do this, I’d encourage you to download this simple FI timeline calculator.

FREE FI TIMELINE TEMPLATE

When you put in your current information, you can see how long it will take you to reach financial independence. You can then enter your updated scenario taking into account a large purchase to see the impact.

The first thing you’ll want to do is ensure that you will reach financial independence by the age of 65 (or whatever your target age is).

If you won’t, a large purchase would likely jeopardize your traditional retirement. In fact, you may want to take steps to increase your savings rate (increase your income, decrease your expenses, or both).

If your timeline would have you reaching FI earlier than the traditional retirement age, that’s fantastic. It’s time to test the new scenario including the large purchase. You can put in the updated information to see how it would impact your FI timeline.

For us, purchasing a campervan that will cost us $120,000 will increase our FI timeline by about 10 months. This is based on our unique data, including our investment balance, savings rate, etc. Not too bad.

Note (for math nerds…): The timeline to FI is calculated by using the NPER (compound interest) formula. When incorporating a large one-time purchase, the formula subtracts that amount from the investing balance. Thus, the change in timeline is approximate. In fact, it slightly overestimates the timeline increase. Why? Because people aren’t likely to sell investments to cover a large purchase. Instead, they are more likely to decrease their savings rate for a period of time to cover the purchase. Since the investments will be left to grow, the impact will be slightly smaller than the formula takes into account.

4. Decide if the Trade-Off is Worth It

Once you know that a decision will align with your values and how much it will impact your finances, you can decide if the trade-off is worth it.

For a campervan, we decided that spending more than $100,000 on a van and conversion would be totally worth it.

Why?

We know it will add so much value to our life. It will allow us to travel and have adventures for weeks or months at a time long before we stop working. Both of these things align with our values.

Will that be worth 10 months added to our FI timeline?

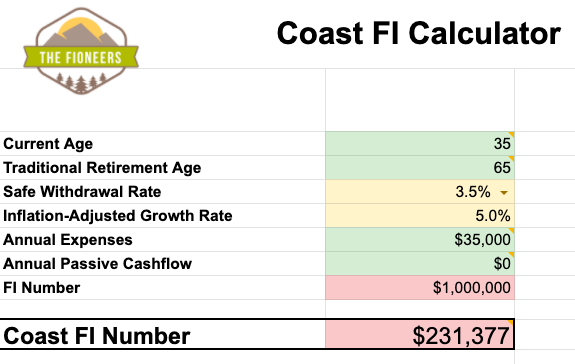

Absolutely! Since we know that we’ve already reached Coast FI, we know we don’t need to save another dime to have a comfortable traditional retirement. In fact, even if we never saved another dime, we could retire at the age of 51 because our current investments would grow during that timeframe.

To figure out your own Coast FI number and timeline, you can download this calculator.

FREE Coast FI Calculator

10 months of a difference makes little impact, especially if we enjoy what we are doing. And, we know that we will still be able to make additional shifts in future years.

And, who knows? Maybe it won’t actually increase our timeline by that much. Maybe we’ll save money elsewhere because of it. Maybe we’ll spend less on travel. Or perhaps, we’ll buy less stuff because we’ll become more minimalist. Or, maybe we’ll even make more money somehow.

Even if none of that happens, it’s still worth it.

5. Determine the Short-Term Logistics and Financial Impacts

Once we determined that the trade-offs were worth making, it was time to focus on the short-term logistics and financial impacts.

These are questions like:

- Do we want to buy a new or used cargo van?

- Do we want to try to build it out ourselves or hire someone to do it?

- Do we want to pay cash or finance it?

- What do we need to do to ensure we have the cash flow needed?

Should We Buy New or Used?

We decided to buy a new van. The principal reason for this is that we knew we’d be investing a lot of money into the conversion. If we were going to invest that much in the build-out, we know we want to van to last as long as possible.

We also knew that it was hard to find good-quality, used cargo vans. Most people use cargo vans for work and drive them into the ground. So, gently used cargo vans are few and far between.

We also knew that we didn’t want to buy a used van that was already built out into a campervan. Why? They are so expensive! You can find a new built-out sprinter van on RV trader for more than $180,000. Used campervans that are ~2 years old will go for more than $140,000. That’s more than we’re planning to spend, and we wouldn’t get to choose our own layout.

Buying a new campervan and doing a custom build will be less expensive than buying a used campervan in good condition.

Do We Want to Build It Out Ourselves or Hire Someone?

We went back and forth about this question. There were really 3 options:

- Try to do everything ourselves.

- Hire someone to do the entire build.

- Hire someone to do the harder parts (electricity, plumbing, framing, cabinets. etc.)

Given that we want to use the van for a trip next summer, we ruled out the possibility of doing everything ourselves. Since Corey still works full-time, it likely would have felt like an additional job.

So, we connected with a van-builder in our area about the possibilities. We wanted to know what were the costs to do an entire build vs. only doing the challenging stuff? Turns out, the challenging stuff takes the vast majority of the time.

The finishes (i.e. the easier stuff that we could easily do ourselves) would take only the last 3 weeks of the build. So, trying to do what would take the builder 3 weeks would only save us about $10,000 and would take us way longer than 3 weeks.

Because of this, we’ve decided to hire a builder to complete the full build for us.

While we think that building out a van ourselves would be fun someday, now isn’t the right time. We’d want to do it when we both had way more free time than we’d need. And, it’s something that we could decide to do later if we wanted to.

Do We Want to Pay Cash Or Finance It?

This was a big question too. At this point, we are planning to pay cash.

We are definitely not anti-financing. If we were to find a loan that has less than a 1% interest rate, we might reconsider our decision.

You may be wondering, “But, why wouldn’t you finance it if the interest rate is lower than the growth rate of the market?”

That is a completely valid question. And, I imagine that my reasoning is the same reasoning why some people decide to pay off their mortgage early (even if it doesn’t make financial sense).

Here’s how our thought process went:

- Our cash reserves are actually larger than we need right now. We wanted to make sure we were prepared for when I took the leap to entrepreneurship. They aren’t enough to cover the full build and keep a good-sized emergency fund, but we can use some of the funds.

- We don’t want another monthly payment that will inflate our spending. Why? We will keep our condo and still have our mortgage. Financing it would increase our expenses over a longer period of time and would make us feel like we need to generate a higher income for a longer period of time. Instead, we want to feel like we can scale back even more over the next few years.

I know that this thought process is based on emotion rather than logic, and that’s okay. That’s why personal finances are personal.

How will we cash flow the van and conversion?

Once we made this decision, we had to figure out the logistics of the cash flow needed to pay for the van and the build.

We like to think of our finances in a fluid way. Recently, one of my coaching clients used a helpful analogy. Imagine you have a hose in your yard. The water running through the hose is your savings. Much of the time, the water is flowing to the largest tree in the middle of the yard. Imagine the large tree is your retirement savings.

You might also decide to plant flowers or a bush on the other side of the yard. Because your tree is established and well-watered, you can water the new flowers and bushes (i.e. your short-term goals) instead for a period of time.

Or, you can get one of those split hoses that will water both of them (but with a smaller amount of water for each). Eventually, the flower and bushes will have the water that they need, and you can move the hose back to the main tree.

This is exactly what we’ll be doing. Since we automate our finances, we simply needed to log in and choose the amount of money to send into our savings account rather than our retirement accounts. Then, once the van build is done and we’ve built up our emergency fund back to a comfortable level, we will automate those funds back to our retirement accounts.

In our case, based on the amount we’ve chosen to re-allocate, we’ll need to do this for about one year. This will allow us to cash flow the campervan and conversion and rebuild our emergency fund. After this, we could decide to plant new flowers (i.e. another short-term goal) or move the hose back to the main tree (i.e. our retirement accounts).

Vanlife, Here We Come!

We are incredibly excited about this new chapter!

As Fioneers, we want the journey to financial independence to be as remarkable as the destination. In fact, we want to take so many small steps along the way, so that when we hit our FI number, it simply feels like another day. We’ll already have built our ideal life. Nothing will need to change.

Buying and building out this van into our tiny home on wheels will take us one step closer to that goal, even as it increases our FI timeline.

If you are interested in learning more about what we included in our van build, we have an updated page with the products we used.

FREE Coast FI Calculator

Congratulations on the van purchase and upcoming build! We have been interested in van life and conversions for some time. I can see the value it can bring to your life and while it’s a big purchase, you’ve thought it through.

We’re considering buying an older Japanese Hiace (or similar) import (has to be 1996 or older due to antiquated US import laws). Something like this. The logistics of making something work with two little kids makes it a bit trickier to find something, but a van like this might just do the trick:

https://www.vanlifenorthwest.com/reimohitop

Best of luck with the upcoming build! Excited to see what you all do with it.

Thank you! That’s a really cool little van! Where are the additional sleeping areas for the littles? Above?

Awesome, I love campervan roadtrips as well!

Nobody could have made the case of justifying a big purchase as well as you did here. Great decision and 10 months delay in FI is VERY manageable! Very well deserved and looking forward to more updates from the road!

Matt

Thanks, Matt! I suppose I should say “intentionality” (or anal-retentive…) is my middle name, so this is a completely normal thought process, lol.

Congratulations Jessica!! I can’t wait to hear more about the van build as things progress!

Thank you Sam! 🙂

Congratulations and good luck! I’m convinced that while we all say that “lifestyle inflation” is bad but we rarely talk about “stress inflation” where if we want to stay at our baseline level of stress, we actually HAVE to spend more money in order to get through the stresses of the day to day life.

We truly deserve it from time to time!

That is so true!

Great going following your heart and not plainly chasing numbers. This is what I think puts you apart from many other FI wannabes. I was wondering why are you not renting out your condo while you enjoy VanLife. This should help big in financing the cashflow.

Hi Rahul,

Thank you for your kind words!

It’s certainly something that we might consider later, but we’d need to do a lot of work to ensure that our space would be rental-ready. For the next couple of years, we’ll be taking shorter trips, so renting our house doesn’t seem as worth it, but possibly later.

We also might consider renting out the van when we aren’t using it on Outdoorsy (at least after a few years when it’s no longer nice and new). That could help with some of the cashflow too!

Best,

Jess

Congratulations on your decision!

I have just spent the last 10 months travelling around New Zealand with my husband in a van. We had an amazing time, of course. But our van was really small and we were always very envious of people with larger vans and campers! Trust me, you will not regret the extra space. Especially when it’s raining. And if your van is more live-in-able, and you’re more comfortable, you’ll spend more time in it and enjoy it more.

Adding 10 months to your retirement journey is basically nothing if you’re going to have a lovely van to travel around in.

Basically all retired people do is travel around in campers here in NZ and Australia! We have been travelling around both countries for nearly a year now. While it has made a dent in our savings, we just feel like we have taken a year of retirement early. Probably 95% of the people we meet on the road are traditional age retirees – and they wish they had done this when they were our ages (we are 40 and 41) because we are fitter and can do a lot more active stuff.

Anyway, this is turning into an essay. But congratulations again and when you’re sitting up at the table in your camper, listening to the rain outside, don’t take having a table and space to sit upright for granted!!!

Hi Aishah,

Thank you so much for your thoughts and well wishes! I’m so glad to hear that you’ve been having such a great time and the encouragement that a larger van was a good choice! We certainly won’t take it for granted!

Best,

Jess

Congratulations on your decision & purchase!

Totally relate to the feeling that you do deserve it instead of feeling guilty that you can afford it.

Looking forward to reading more of your upcoming adventures in the van. I’m very attracted to tiny homes but not sure of the logistics of where to park it etc

Hi,

Thank you so much for your well wishes. We will definitely share more about what we learn!

Best,

Jess

Wow! Forgive me if you’ve done this already (I’m new around here), but will you please do a follow up for us at some point? No pressure and no worries! I’m just so curious to hear how it goes for you over time.

There’s always something unforeseen (positive or negative and hopefully the former) that comes up and I’ll be curious to hear your take.

Lastly, I appreciate that you are embodying a consistent theme that I’ve been hearing from people that reach FI. There’s a “now what?” component that keeps cropping up, and it sounds like you’re really making it a point to enjoy the slow fi ride.

Great stuff!

Hi Mr. D,

Yes! We will definitely be doing a follow-up at some point. The van is actually with the builder right now, and we’ll finally be getting it in 3-4 weeks! We are so excited. We have our first camping trip planned for Memorial Day weekend. We’ll definitely write about it.

Best,

Jess