Before I learned about financial independence, I was drifting. I didn’t know what I wanted out of life, and I didn’t think it was worth trying to figure it out.

When I graduated from college, I had unconventional dreams. I wanted to travel the world, do international development work, and help people achieve economic mobility. A few years into my career, I no longer believed that my big goals were possible.

I didn’t feel like I was qualified to do any of this, and I could barely make enough money doing it.

I graduated in 2009 into a period of economic downturn. Jobs were scarce. It was all I could do to find any job – let alone a job that would allow me to have an impact in the world I had hoped for.

I suppose my first couple of years in the workforce were “unconventional.” I did street canvassing for a charity in New York City for a year. This meant I was outside all day in the rain, snow, and heat trying to get random people to donate.

Then, I did a year-long AmeriCorps program in Newark, NJ. During this program, I worked in a nonprofit and received a living stipend. The stipend was 105% of the poverty rate for my county, which came out to about $11,000/year before taxes.

Once I finally landed a real job in a nonprofit organization, my perspective had shifted. I was no longer going after my dreams. Working in a nonprofit was the closest I’d ever get to them.

After this, my life became a conventional story. I worked 40+ hours/week and was always chasing the next promotion. This is what I was supposed to do, I reasoned. I never wanted to be in the same financial situation as we were in 2010.

Yes, I was working toward a cause. Yet, the recognition and extra income from the next promotion was the drug that kept me going.

I got to a point where I was working 50+ hours/week consistently in a toxic work environment. I was also commuting 45 minutes each way. I was completely exhausted, and I had disillusioned myself into thinking that it wasn’t so bad. Nobody really liked their work, did they? This was fine… for a job.

Hindsight is 20/20. Looking back, I see how bad it actually was. I started to experience burnout and severe anxiety from intense work demands. I became depressed. It was painful to realize how far off I had gotten from what I actually wanted out of life. It was even more depressing that I didn’t believe any of it was possible.

I didn’t know who I was anymore. I didn’t know what I wanted, and I didn’t believe it was possible to get there.

Financial Independence Re-Introduced Me to My Goals and Dreams

When I first learned about financial independence, I thought it would be the answer to all my problems.

I was burned out and exhausted. I had no idea what I wanted to do. I had a hard time answering this basic question from Your Money or Your Life, “What would you do if you didn’t need to work for a living?”

I was so burned out that all I wanted to do was take a break and sleep for a year. I also realized that it took a lot of mental energy to think about it because it was painful. It showed me how far away I’d strayed from what I actually wanted out of life.

Once I got past some of the pain and exhaustion, I was able to start thinking about what I wanted. I still couldn’t fathom wanting to do anything where I’d need to make an income. Maybe once I was no longer burned out, I would want to volunteer or learn advanced photography.

Financial freedom felt like it was all or nothing. I was either financially independent, or I wasn’t.

I thought the only path was to stay in traditional employment for the next 10 years until I could retire. Then, I could do the things I wanted.

Financial Freedom isn’t All or Nothing

In the summer of 2018, I began to have severe anxiety and panic attacks. It wasn’t until we started looking at the specifics of our situation that I realized financial freedom is incremental.

I knew that we had always prioritized saving, even when we were only able to save a small amount. We lived within our means. We did everything we could to not take on debt, even for undergraduate and graduate school. I know we were doing “well” financially, but I wasn’t really sure what that meant. It all still felt like monopoly money to me.

I was faced with two scenarios:

- I could quit my job, take time off, and find another job after I had improved.

- I could take a leave of absence and apply for disability insurance through my employer.

By looking at our financial situation with new eyes, I realized two important things.

- We had 9 months of expenses saved in our emergency fund. This meant that we could both quit (or lose) or jobs, and we would be able to cover our expenses for almost a year without digging into our investments. This was unlikely to happen because Corey enjoys (and is quite good at) his job.

- We were already saving about 50% of our income. This meant that I could quit my job, and we could live on Corey’s income indefinitely until I was ready to go back to work. We wouldn’t be adding more to savings, but we wouldn’t actually be drawing out of our emergency funds or investments either.

Because of my early career experiences, I lived with a scarcity mindset. Having this level of financial security was unfathomable to me until I sat down and put numbers and timeframes to it.

Ultimately, I decided not to quit. While I could quit, I decided to make use of the disability benefit provided by my employer. I took 6 months off of work and received 60% of my salary from disability insurance. This allowed us to continue working toward our financial goals and have no money stress while I was recovering.

I wish I hadn’t gone through this experience of burnout. At the same time, I am happy that it opened my eyes to our financial situation and the ways that money can provide freedom before FI.

While unpleasant, I learned a lot from the situation. I learned that I could use my financial freedom to make my life better now. I didn’t need to wait until I reached full financial independence.

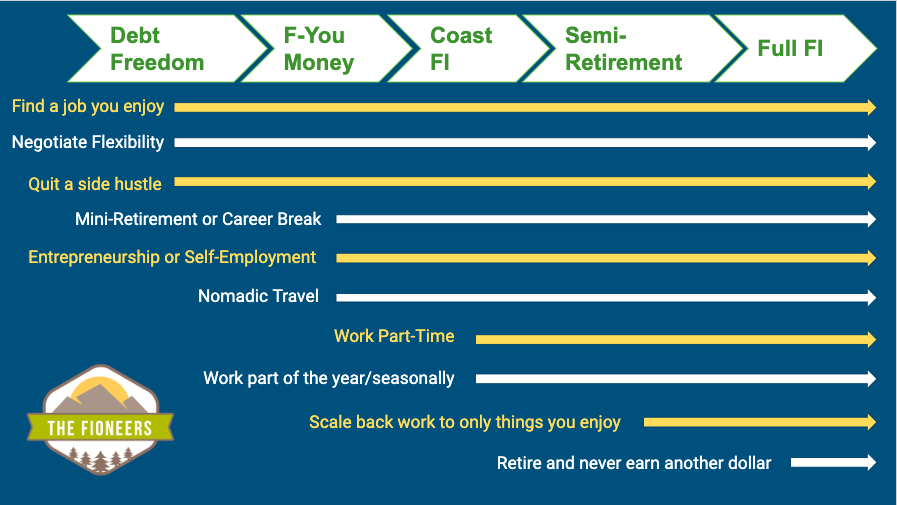

Stages of Financial Freedom

Armed with this new realization, I spent a lot of time learning about different ways people are using financial freedom in their lives now. From these countless stories, I’ve realized that there are 5 common stages of financial freedom.

1. Debt Freedom

People define debt freedom in different ways. I define debt freedom as having no debt beyond a mortgage payment. Our monthly mortgage payment is lower than what we’d previously paid in rent (and it has a low-interest rate). So, we have decided to not focus on paying it down quickly.

Debt could include student loans, medical debt, credit card debt, etc.

The great thing about being free from debt is that it can dramatically reduce your monthly expenses. In 2017, we became debt-free beyond our mortgage. We had a loan that we used toward our down payment for our condo. When we became debt-free from this loan, we reduced our costs by about $9,000 per year.

When you don’t need to reserve a certain amount of money each month to pay down debt, you don’t need as much money to live on. More money can then be funneled to savings, or you can choose to make a lower income.

2. F-You Money

F-you money is when you have enough cash on hand in an emergency fund or liquid investments to:

- Allow you to walk away from a toxic situation (job, relationship, living situation, etc.), or

- Give you the confidence to go after or ask for what you want

F-you money can allow you to walk away from a toxic work environment or an abusive relationship. It can allow you to negotiate for flexibility or take the risk to become an entrepreneur.

The important thing to know about f-you money is that it must be combined with a feeling of freedom. If you don’t understand your financial situation and how much freedom it can provide, you will never feel like you have f-you money.

This was true for me. I needed to understand what having an emergency fund and a high savings rate meant for our lives.

Only then did I start to feel the power that f-you money can provide.

3. Coast FI

Coast FI is when you have enough invested for a comfortable traditional retirement if you don’t touch it until then.

When someone reaches coast FI, this means that they only need to cover their actual costs of living until they retire.

When you reach Coast FI is based on your age and the amount of money that you expect to need in retirement. The amount of money you need to have invested to be coast FI is actually much lower than I would assume.

For example, you know a 30-year old who spends $40,000/year who would like to retire at 60. This person only needs about $160,000 invested at the age of 30 to be considered Coast FI. That means they could find a job they enjoy or reduce their hours because they would only need to make $40,000/year.

Obviously, these numbers differ depending on your age and your time horizon.

If you would like to understand your own Coast FI number, sign-up for our newsletter to receive your free FI Milestones Calculator.

FREE TEMPLATE

Corey and I reached Coast FI in 2019. We haven’t scaled back to cover only our costs of living since we would like to reach FI and have the ability to retire early in our 50s. Reaching coast FI allowed us to start making shifts. I started working part-time (3 days/week). This allows me to focus on my health, passion projects and having a balanced life.

Corey could also scale back work at this point if he’d like to. He currently enjoys his work and wants to keep working full-time for the foreseeable future. We aren’t yet taking advantage of the full benefits that coast FI can offer.

4. Semi-Retirement

After reaching Coast FI, you can also continue to build up your investments, like we are doing. This could allow you to live a semi-retired lifestyle. We define semi-retirement as a period where someone only needs to cover part of their cost of living with active income.

Let’s talk this through with an example. Let’s say someone has $1,000,000 in their investment accounts. This would allow them to draw down $35,000-$40,000/year without depleting their assets. If their total expenses were $50,000/year, they could choose to supplement their investment income with $10,000-$15,000 of active income. They would likely want to earn a bit more than this so that they don’t need to withdraw a full 3.5-4%. This would allow their portfolio to continue growing so that it could cover their full expenses in the future.

Someone could fairly easily generate $10,000-$15,000 per year through a side hustle, walking dogs, or doing a fun part-time job.

We’d love to be semi-retired someday. We’d love to run our own business and have it cover our full expenses while we are coast FI. If we could scale back later and live a semi-retired lifestyle, that would be ideal.

5. Full Financial Independence

This is when passive income from investments can completely cover your cost of living. At this point, you can choose to retire and no longer work for income.

We eventually want to reach full financial independence so that we no longer need to work for money. I’d like to reach FI by our 50s because there are so many unknowns later in life.

If we kept our life (and savings rate) the same as it is right now, we could reach full financial independence in 8 years. It’s unlikely that we won’t make changes to our lifestyle between now and then. We aren’t racing to the finish line since we enjoy our current lives now.

Lifestyle Design Options Available at Different Stages of Financial Freedom

There are so many lifestyle design options that are available to us along our journeys to financial independence.

Let’s talk through the options at each stage. Within each stage, I will share the options available. Please note that each option discussed is also available at the later stages. Depending on your situation, some of the options might also be available earlier as well.

1. Debt Freedom

Once you become debt-free, there are so many options available to you.

- You can find a job that you’d enjoy more.

- You can more confidently negotiate flexibility at work, such as working from home.

- You could also decide to quit a side hustle. If you had a side hustle that was helping you pay back debt, you could choose to quit when you no longer needed the income.

2. F-You Money

Once you have a certain level of savings, there are many more options available to you.

- You could take a mini-retirement or a career break.

- You could transition to entrepreneurship, self-employment, or freelance work.

- You have more freedom to pursue creative endeavors that could have a more irregular income. If you have a buffer you can sustain both a windfall and a draught for periods of time.

- You could become a digital nomad. Remote work, self-employment, and entrepreneurship all support this lifestyle.

3. Coast FI

Being Coast FI can provide you with even more options. At coast FI, you could decide to reduce your income to only cover your expenses. This could allow you to work part-time like I do. It could also allow you to work for only a part of the year.

My favorite example of someone who is Coast FI is Michelle who writes the blog Frugality and Freedom. For the last several years, Michelle has worked for part of the year and she travels the rest of the time.

4. Semi-Retirement

Being semi-retired provides you with even more options. At this point, you can scale back work even more and spend time doing only the things you enjoy.

For example, I have a friend who I met at my Choose FI local group who is planning out her semi-retired lifestyle. She has enough investments that she could cover her entire lifestyle except for $10,000/year. She is toying with ideas such as walking dogs for 5 hours/week or doing some other consulting work or side hustles. This would enable her to spend the vast majority of time doing things she loves, like hiking, skiing, and making an impact on the world around her.

5. Full Financial Independence

When you reach full financial independence, you have the option to retire and never make another dollar. Surprisingly, this is the only lifestyle design option that is not available in any other stage.

Most people, including my younger self, assume that you need to be FI before you can do many of these other things (nomadic travel, work part-time, start a business, etc.). This just isn’t the case.

If you want to read more stories of people living their best lives before FI, check out our Slow FI interview series.

Why You Should Design Your Life Before Financial Independence

There are many people who have gone down this financial independence path before us. I want to make sure I listen to the wisdom that these people want to pass on to us.

I recently asked Tanja Hester (author of Work Optional and blogger behind Our Next Life) what she would have done differently on her financial independence journey.

Here is what she told me, “I’d go more slowly and use all my vacation time. I would say yes to once-in-a-lifetime trips we could have afforded but skipped to meet aggressive savings goals. Everyone pursuing early retirement seems to understand that time is in limited supply. But, we sometimes act as though only future time is precious and current time can be squandered in the interest of saving.”

Carl, who writes at 1500 Days, calls his approach to achieve to FI a “death march” and urges his audience to take a slower path.

Robert, the writer behind Stop Ironing Shirts, reached financial independence in 2019. He wishes that he’s slowed down his career to focus on his lifestyle when he’d reached Coast FI. He now recommends his readers to take a more balanced approach.

Joel, who writes at Financial 180, retired early in 2017. After 16 months, he decided to go back to work. When he wrote about that decision he said, “It wasn’t ‘work‘ I hated with a passion. It was lack of a work-life balance. It was mandatory unpaid overtime. It was the lack of control I had over my time and stress levels. I didn’t hate work in general; I hated my specific job… I should have quit sooner.”

There are many lessons we can learn from the wisdom of those who have gone before us:

- We will never get our lives back exactly as they are today. I will never be 32 again. If you have kids, they will grow up fast and they will never be the same age as they are again. The situations of our friends and family may change. We need to live every moment to the fullest, so we don’t miss it.

- Our lives are not guaranteed. Imagine spending 10 years pushing hard toward financial independence. During this time, you let important things in your life (family, friendships, mental health, etc.) suffer. What if you were then diagnosed with a terminal illness? You wouldn’t be able to enjoy the fruits of your earlier labor. Would you have regrets? We don’t know what our future holds, so it’s important to balance saving for the future with living a full life today.

- For most people (after getting past burnout), their ideal lives include meaningful work. After decompressing from burnout, many early retirees realize that work is part of their ideal life. Some go back to work for employers. Some do work for themselves. Many continue to make an income. If I could make an income doing things I enjoy, I’d regret not transitioning sooner.

These are only a few of the reasons why we should design our lives while we are pursuing financial independence. Don’t wait until you’ve reached FI to figure out what you want.

You Can Both Pursue FI and Live a Fulfilling Life

The most amazing about saving money toward financial independence isn’t that we then can use the money to retire early. Instead, we can use the financial freedom we gain along the way to live happier and healthier lives, do better work, and build strong relationships.

Some people believe that saving for the future keeps you from living an awesome life now. In reality, it’s the opposite. Saving for the future is what allows me to live an awesome life in the present.

To Live a Fulfilling Life, You Need to Know What You Want

A big thing that holds a lot of people back from living a fulfilling life is that they don’t know what they want. Don’t wait until you have reached FI to do the work to figure it out!

If you do, you might miss out on opportunities to live your ideal life along the journey.

Over the last two years, I’ve gone through a path of discovery to figure out the core things I want from life. They are:

- Location Independence. I want a home base, but I also want to have the ability to travel for months at a time.

- Teaching/Mentoring – I’m a learner at heart. My learning process isn’t complete until I can share what I’ve learned with others. This brings me a lot of fulfillment.

- Balance – I want to ensure that I focus on staying mentally healthy, have time to relax, and build strong relationships.

- Creativity – I want to have the time and energy to focus on creative outlets like writing.

After a lot of reflection, I realized that I do not need to be financially independent to incorporate any of these into my life. In fact, I have three of them already.

Because I have reached Coast FI, I work part-time in a nonprofit. This allows me to have the balance that I want to stay mentally healthy and build strong relationships. It also provides me time for creative endeavors, like this blog. I also have the opportunity to share things I’ve learned through my blog, my coaching business, and my day job.

The only goal I haven’t yet reached is location independence. I don’t need to reach financial independence before I can achieve location independence. I am working to build up my own online business that I can do from anywhere. Another option I have is to negotiate a super flexible work arrangement. This might allow me to have longer stretches of time off to allow for extended travel.

How to Design Your Life: What Do You Want Out of Life?

Knowing what you want doesn’t happen overnight. For me, it was a 2-year process of reflection and exposing myself to new people, ideas and lifestyles. I’m sure my vision will also continue to evolve as I experiment and learn more about what I want.

If you are struggling to figure out what you want, I’d encourage you to download my free guide: Top 6 Questions to Figure out What You Want. I’d encourage you to use these as journal prompts and/or use them as a discussion starter with your partner or a trusted friend.

FREE QUESTIONNAIRE

I’d love to hear from you! Where are you on the financial independence continuum? How could you live the life you want along the way to FI?

Thanks for posting this, especially the part about taking the leave of absence. I let personal pride get in the way when I should have done this for at least the three months allowed prior to quitting.

Hi Robert,

Thanks for the comment! I wish that it was more acceptable to attend to your mental health. No one would think twice if you were attending to something physical-health related. This is definitely something I try to make people in my organization aware, so they can take time off.

Are you feeling recovered from burnout yet? Now that you’ve been early retired for almost a year?

Best,

Jess

This post is so timely! As you know Jess, it was my first day back at work after a month of vacation and today I truly cherished the freedom I’ve built into my path towards FI. The return felt extremely smooth as I returned to my comfortable work from home routine.

I also think that taking time in the past to work through those questions you mention, and that “what would I do if I didn’t need to work” question helped put my current work into better perspective. As we get closer to FI, I’ve made moves in my work to find more freedom and to simply align it closer to this life I want. I like to do work which I feel makes a good impact as long as it is efficiently done… This has helped me increase my organizational skills at work. More importantly, if I leave for an extended period on vacation as I just did, it makes it easier for anyone replacing me to take over some of my work as everything is clearly detailed and documented.

It truly is such a powerful thing to take the time to design your life before reaching FI! I’m looking forward to seeing where your own freedom leads you :).

Hi Ms. Mod,

Thank you so much for the comment! I’m so happy that you feel like you’ve been able to take advantage of this awesome freedom to take extended time off and to work from home! You are such an inspiration, and I’m excited to see where your freedom leads you!

Best,

Jess

Great article. I never considered Coast FI as an option, but realize after reading tour article I have reached this goal. I’m not going to slow down my pace like some of the folks you mentioned suggest. I’m ramping it up as much as possible. My goals aren’t (currently) for me to reap the rewards of. I made a decision a while back that I want to create generational wealth. I always thought how great it would’ve been to have wealth handed down to me at some point. It’s not going to happen. So I decided that I’ll be the one to start it and teach the kids about money and investing so the family won’t have to start from $0 going forward.

Side note: Your site looks really nice. I like your layout and the way it flows. Great job on it!

Hi Jared,

Thanks for the comment. I can absolutely understand your motivation to create generational wealth. Since you’ve already reached Coast FI, I imagine as you get further along in your journey there will be ways for you to both improve your life and create generational wealth. I imagine it won’t be an either/or scenario. 🙂

Best of luck to you!

Jessica

Very thoughtful write up here! I agree with the stages. Speaking from experience, it was sooo much harder to get through the first four years of the FIRE journey. It wasn’t until the mortgage got paid off after year four that I started to get comfortable with my job situation. Then a promotion struck, and I’ve just recently cleared the last financial hurdle to F-You money. Irony is that I kind of like the gig now – funny how time, experience and F-You money can keep you coming back!

Having kids does make things tricky. I’ve discovered though that once they start up grade school, they start down their own path. We dedicate most of our time outside of work to them, so we don’t feel that we’re missing out. It won’t be long before they opt to spend more time with friends vs. their parents, so it seems to me there’s a magic period of being there more for them – infancy to age 8 or so, then they need to start cutting their teeth on the real world.

Hi Cubert,

Thanks for the comment! I wonder if you could share the difference that you feel between F-You Money and Coast FI. Based on what I know you, I’d assume that you are already Coast FI, but it sounds like you didn’t feel like you had F-You money until more recently. You also may have been Coast FI before paying off your mortgage.

I’m fascinated by this! I’d love to learn more!

Jessica

I just stumbled on your blog from either /r/CoastFIRE or /r/financialindependence, and just wanted to say this was an incredible post!

It encapsulated something I’ve been pondering, that rather than an “all or nothing”, FIRE might be more of a continuum, in that as you move closer to your FIRE number, more things become possible, such as working part-time or pursuing passion projects.

Especially with the pandemic, with the job market tightening up, it pushes back FIRE for a lot of people, but it’s great to think about the steps along the way, and realize that there might be possibilities that don’t require full-fledged FIRE.

Hi John,

I’m so happy you found us! I definitely think of FIRE as a continuum, where every dollar we save, the more freedom we have.

I wish you the best! Let us know if you have any questions.

Jessica

Great post Jessica.

A recent email I received bought me here 🙂

I love the graphical illustration and for me, its actually trying to grow that side hustle to a level where I can back off the day job and have F U money.

Difficultly with learning about FIRE and the different methods just seems to be that life changes can dramatically alter the goalposts (having kids, buying a house, etc). Still trying to work out that magic number!

Thanks,

Cem

Hi Cem,

That’s a great goal. I agree – things can always change, so it’s important to stay flexible! That’s why I like Slow FI so much. We’ll continue to generate income after we design our ideal life, so it takes a lot of the pressure off!

Best,

Jess

I wish I knew this lesson many years ago. When I discovered FI, I knew there was a path to escape the stresses of my demanding job.

I thought there was only one path, an all-out press for FI.

Today, I enjoy the benefits of FI through a mini-retirement. I’m well beyond the F-you money stage, though.

Had I realized ditching my stressful job was possible, I would have done so, long ago.

Hindsight 🙂

Thank you for sharing your message. The journey to FI doesn’t have to create tension in our lives.

You’re reaching people and changing perspectives for the better.

Hi Topher,

Thank you so much for sharing your story, and I’m so glad that you have the opportunity to take a mini-retirement. I hope that you’ll find a new job once you go back to work. 🙂

All the best to you,

Jessica

Hi, Jess,

My 36-year-old daughter introduced me to FIoneers. She is married to a stay-at-home husband who is the primary caregiver to their 4-yr old daughter and 21-month old son. They have a pre-school expense of $700/month and rent of $2300/month, she makes $130K/year as a neuropsychologist. She has quit her current job to take a 3- month unpaid sabbatical. They will live with me and my husband for one month and with my son-in-law’s mother for two months. My daughter values highly family time and children being with grandparents. She and her husband love backpacking and hiking the major trails in the US. She may have thought of a sabbatical for mental health before reading your online advice. You helped her give herself permission to do it, and for that I thank you.

My husband and I followed the traditional Baby Boomer work-straight- through until you retire scenario. We missed so much by doing that, and now I have health problems that limit my mobility. Live life while you can!

Hi Elaine,

Thank you so much for your kind note. I am so happy to hear that your daughter can take a sabbatical that will support her mental health. Thank you so much for sharing your wisdom also.

Jessia