Kiersten and Julien of Rich and Regular have been my content creator role models from the very beginning. They were one of the first blogs I started to follow in 2018 when I launched the Fioneers.

I had the opportunity to meet them at a 2019 conference. They had just won Blog of the Year, and I knew I wanted to soak up everything I possibly could from them. The thing I was most impressed by was the obvious love, care, and respect for their audience. I wanted to emulate that.

When I learned about their new book, Cashing Out, I was ecstatic! If their content up to this point was any indication, their new book about FIRE was going to be LIT (pun intended…).

I reached out to get an advanced copy, and it did not disappoint.

While their message is specific to Black Americans, I believe so much is relevant to anyone who experiences oppression related to any identity characteristic, such as race, ethnicity, gender, gender identity, sexual orientation, disability status, etc. In fact, I found the advice and recommendations relevant to me, particularly as I reflect on my identity as a woman with chronic health challenges.

What is “Cashing Out?”

The typical FIRE narrative focuses on the mechanics of reaching FI, including:

- Earning more

- Spending less than you earn

- Saving and investing the difference

- Retiring early to a life of eternal bliss

Cashing out goes beyond the typical FIRE narrative.

Cashing out affirms that both money and our identities impact every aspect of our lives.

It also asserts two important and seemingly paradoxical beliefs:

- There are systemic issues faced by certain populations of people in our country.

- It’s possible for these same people to position themselves to benefit from the system without endorsing its flaws.

Cashing Out speaks directly about the systemic barriers that Black people face. I believe these same principles apply to other identity characteristics as well.

Here are Julian and Kiersten’s words on what it means to cash out.

“In this book, we’ll tap into your innermost motivations to build real wealth, provide you with clear guidelines to break free from required work on your own terms, and lead you to an end goal with your dignity and retirement portfolio intact.”

AND

“If the fight you’re in is rigged, what’s the minimum amount of rounds you need to hang in there before voluntarily throwing in the towel? Then, instead of doubling down on your career ambitions, ask yourself how quickly you can hop off the rickety ladder we’ve all climbed onto.”

Cashing Out is about acknowledging the situation in our world as it is (not as it ought to be) and behaving accordingly. It’s about figuring out how to opt-out of an oppressive system as quickly as possible. This will allow us to make it to our end goal with our dignity and retirement portfolio intact. Then, we’ll have the time, energy, and confidence to work toward real change and to “speak without fear of risking [our] financial livelihood.”

Why Cash Out

According to Julien and Kiersten, there are as many reasons to cash out:

- To have more time to do the things you enjoy

- To be safe from layoffs or corporate change

- Increase your likelihood of success (and do it on your own terms)

- Be present for your family

- Freedom from burnout

They presented freedom from burnout (and improved mental health) in a very compelling way by discussing how the standard of Black excellence can be damaging. While on the surface, Black excellence implies a positive message, it actually “upholds a system where Black people have to work twice, three times, even four times as hard to earn allowances that other folks receive as a birthright.”

In the book, Julien and Kiersten write, “The standard of black excellence isn’t worth it if it costs you your sanity and your well-being. You deserve to live a life that is designed to put your needs ahead of the endless list of unsolvable problems that work forces on you.”

This statement gave me chills as I read it because it is so true!

As a woman, this message rings true for me. I used to believe that I needed to work twice as hard and prove that I could climb the corporate ladder and be as successful as any man. And, it ruined my mental health. In 2018, I started having severe anxiety and panic attacks and needed to take 6 months off of work to recover.

When I learned about FI (and so many new ways of living), I realized that I could put my needs first. My goal was no longer to climb the corporate ladder, it was to “cash-out” of the toxic system and design a life I truly loved.

How to Cash Out

In the book, Kiersten and Julien encourage us to aim for a 15-year career.

To do this so quickly, someone would need to have a fairly high income to start with. But, even if we can’t cash out by the age of 37, they share some valuable tactics to help make it possible. These include:

- Giving your income a purpose

- Investing wisely

- Building multiple income streams

- Find Your People

1. Give Your Income a Purpose

I absolutely loved the idea that you need to give your income a purpose. In their words, “When your income lacks purpose, you’re vulnerable – vulnerable of being sucked into the system of consumerism and the endless work culture.”

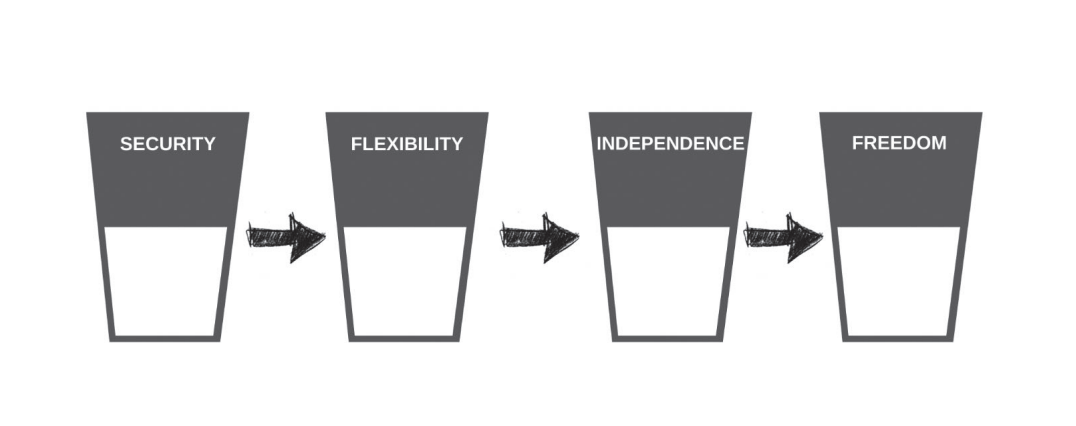

In the book, they outline that there are 4 purposes of income.

The first purpose of income is security. Security means that you are working toward meeting your needs (even if it’s not the nicest version of getting those needs met).

The second purpose is flexibility. Once your needs are met, you have the opportunity to spend more to give you a better lifestyle. I’d also add if your needs are met and you want flexibility, you could also choose to work less.

The third purpose of income is independence. Once you have flexibility, it’s important to “make the mindset shift from seeing your income as fruit you can enjoy today to seeing your income as seeds to be planted for tomorrow.” This is critical for retirement planning. When you start to put your money toward gaining more independence, it can provide you with a lot of options.

In the book, they discuss different levels of independence:

- Low Independence (or Coast FI): The point at which you no longer need to save for traditional retirement. The money invested will already grow to provide you with a comfortable traditional retirement. This means you only need to cover your actual costs moving forward

- Mid-Independence (or Traditional FI): The point at which passive income will cover your full expenses and you never need to work again. This is often defined as twenty-five times your annual expenses.

- High Independence (or Fat FIRE): When you have more than 25 times your annual expenses and would never need to worry about overspending.

The last purpose of income is freedom. They define this as the point where you feel like you have the freedom to do the things you want like:

- Walking away from a toxic job or an abusive relationship

- Taking time off work to support your health or simply to have an adventure

- Being able to support your aging parents

I love the way that Kiersten and Julien articulate the purposes of income. It reminds me in so many ways of what I think of as the continuum of financial freedom. Where different levels of financial freedom are unlocking new lifestyle design options for you.

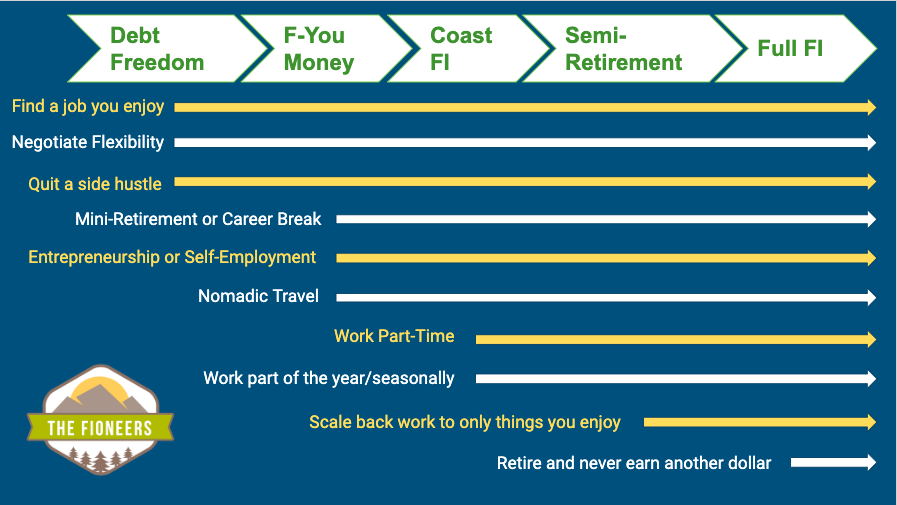

My one critique here is that I don’t think freedom needs to be its own separate bucket. Instead, I think of it as gaining freedom as you move through each stage regardless of whether you are thinking about it in their framework (security → flexibility → independence) or ours (Debt Freedom → F-You Money → Coast FI → Semi-Retirement → Full FI).

2. Invest Wisely

As most people within the financial independence movement would agree, investing wisely means investing in index funds. Funds such as Vanguard Total Stock Market Index Fund (VTSAX), the S&P500, or Fidelity’s Zero Total Stock Market Index Fund (FZROX) can be found within almost any financial institution and within your employer-sponsored retirement accounts.

These types of funds have extremely low management fees. And, when you learn how to invest without the oversight of a financial advisor, you get to keep a lot more of your hard-earned cash and the growth that comes from it.

As we’ve learned, actively managed funds don’t usually beat the overall growth of the stock market, so why pay what could amount to hundreds of thousands of dollars in management fees simply for an educated guess.

In the book, they illustrate the incredible amount that fees can take from your portfolio. Here’s an example they shared in the book.

Say you invested $10,000 and you were paying 1% in fees. 1% doesn’t sound like a lot, but over the course of 40 years, it adds up. In the end, your $10,000 would be worth $150,000, but you would have paid $48,000 in fees (almost ⅓ of the value!).

If you were to, instead, invest that $10,000 in an index fund with a fee of 0.04%, you would have only paid $2,000 in fees. You’d end up with $46,000 more dollars in your pocket.

This is why it’s so important to pay attention to the fees charged by the funds.

3. Build Multiple Streams of Income

Kiersten and Julien are big proponents of building multiple income streams, particularly in the digital economy. Rather than waiting for your boss to promote you, they say that we can all start earning our own money now, outside of a normal 9-to-5 job.

They encourage people to look at side hustles in a matrix of urgency vs. upside.

- Urgency = How quickly do you need to money

- Upside = How much could it grow over time (i.e. is it scalable without putting more time in?)

They shared a few examples of side hustles:

- Getting bank bonuses – high urgency, low-upside

- Working in the gig economy (e.g. Uber, Doordash, etc.) – mid-to-high urgency, low upside

- Arbitrage or flipping goods (i.e. buying low and selling high) – low urgency, mid-to-high upside

- Digital content, products, and courses – low urgency, high upside

I’d add a few more possible side hustles to this list, including:

- Creating physical products and selling them online or in a brick and mortar shop (low urgency, low-to-mid upside)

- Offering services in the freelance economy (e.g. writing, virtual assistant, community management, proofreading, etc.) – mid-urgency, mid-upside

- Offering a service directly to customers (e.g. personal training, coaching, dog walking, personal chef, etc.) – mid-urgency, mid-to-high upside

In the book, Kiersten and Julien encourage people to embrace the digital economy. While that is important, I would also encourage people to consider what activities they would really enjoy doing.

When I started to focus on generating income on the side of my day job, I knew I wanted to do something I enjoyed and was passionate about. That’s why I call what I do a “passion hustle.” It’s what I’d do if I didn’t need to work for income. The fact that it earns me income is a bonus that allows me to transition to my ideal lifestyle before reaching FI.

4. Build Your FI Community

Kiersten and Julien are huge proponents of building a community that supports your FI journey.

They say, “When you make the life-changing decision to cash out, you aren’t just leaving a job behind. In some ways, it may feel as if you are leaving an entire community behind. You’ll begin to feel as if people see you differently, and in some cases, it’s because they do.”

I wholeheartedly agree. This is why it’s so important to build a community with like-minded people. These people will encourage you along your desired path and not make you feel like you are making radical (and also terrible) decisions.

One huge benefit of being part of a community is that you start to encourage and believe huge dreams are possible for the people in your community. After a while, you start to ask… “Hmmm… why can’t I apply those exact same beliefs to myself?”

Your FI community will help you dream bigger and build the confidence to take action.

Start Using The Freedom You Gain Long Before Reaching FI

One thing that I loved about this book and the concept of cashing it is that it doesn’t focus on getting to the FIRE finish line as quickly as possible.

They say, “Appreciate the journey to achieving your stated financial goal. So many benefits people are really looking for can be utilized and experienced long before achieving their ultimate goal.”

I wholeheartedly agree. Financial freedom is not all or nothing. You don’t have to wait until you reach full financial independence before taking advantage of the flexibility and freedom it can provide.

A few ways I’ve used my financial freedom along the path to FI include:

- Taking a 6-month career break in 2018 to deal with a health issue

- Going back to work part-time and working 3 days/week for 2 years

- Starting a passion-based business on the side and eventually taking the leap to entrepreneurship

- Buying and building out a campervan that will support our goal to become location independent.

Kiersten and Julien have done the same. The biggest step they took was quitting their jobs in corporate America and becoming entrepreneurs long before reaching FI. To learn more about their story, I would 100% recommend buying a copy of their book Cashing Out. You can also check out the Slow FI interview with Kiersten about quitting her job in 2021.