My first exposure to Gwen from Fiery Millennials was a MarketWatch article about people who “failed” at early retirement.

When I first read the story, I was very confused. It said that Gwen tried to “retire early” with ~$200,000 in investments and savings.

My first thoughts went something like this: “In what world would this amount be enough for someone in the United States to retire early? Well, of course, she’d have to go back to work…”

Of course, this feeling of superiority was what this article was trying to elicit from readers. I quickly figured out this wasn’t the REAL story.

The article was a huge misrepresentation of Gwen’s experience.

At the age of 27, Gwen did not say she was “retiring early” with a nest egg of only $200,000. She was actually just experimenting with a new lifestyle design – freelancing and running her own business. This is a completely viable career option and lifestyle design, regardless of whether someone wants to retire early or not.

Although this new lifestyle design didn’t work out for Gwen, I would call the experiment a success – NOT a failure.

Gwen had the courage to try out something new. Once she realized that she didn’t like the crazy hours, the stress, and the feeling of always needing to be working on something, she decided to try something else.

Gwen didn’t fail. She learned an extremely valuable lesson about herself and what she wanted out of life.

Gwen reached out to me recently. She’s gone back to full-time work and has decided to quit almost all of her side hustles that were causing her stress.

Of course, I wanted to learn more about this decision.

Gwen, like so many people, made a decision to prioritize her quality of life over the pace at which she can achieve financial independence.

Some people have done this by quitting stressful side hustles. Others have chosen to travel the world, work part-time, take a job they enjoy even if it pays less, or live a semi-retired lifestyle.

Let’s hear about Gwen’s story!

1. Tell me a little bit about you.

Hi! My name is Gwen. I’m 28 and I recently moved to the DC area.

I found FIRE when I was a junior in college and embraced everything about it. I saved as much as I could and tried my best to keep my expenses low.

I grew increasingly dissatisfied with that lifestyle, though, so in the spring of 2018, I quit my cushy IT job and tried to make it as an online influencer/entrepreneur.

This didn’t work out for a variety of reasons, so in late 2018 I went back to full-time (W-2) work.

2. What deliberate decision have you made to slow down and improve your life? Why did you decide to make this decision?

After I realized I’m better suited to full-time work in a company, I realized I couldn’t keep hustling 24/7.

The hustle was intense. At one point:

- I was a long-distance landlord

- I ran an Etsy Shop, a blog, and a podcast

- I was freelance writing and doing virtual assistant work

- I dabbled in financial coaching

I was miserable.

I slowed down a bit when I went back to work.

I got rid of the rental property, freelance writing, and financial coaching.

My quality of life improved, but it wasn’t quite enough. My brain felt like it was stuffed with knowledge and things I had to care about. I couldn’t enjoy life if I was constantly thinking of ways to improve my various side hustles.

In May 2019, I divested myself of every side hustle except the blog and the Etsy shop. The Etsy shop is on set-and-forget mode and requires little to no effort. Since the blog brings me happiness and improves my quality of life, I decided to keep it.

I also made a deliberate decision to slow down on the amount of money I save each month. In my last W-2 job, I maxed out my 401(k) and my HSA and put money into my Roth IRA.

At this point, I am putting just enough into my 401(k) to receive the employer match. I am also putting a bit into my HSA, but I am nowhere near maxing out either account.

I now live in a much higher cost of living area, so my expenses are quite a bit higher than they were in the Midwest.

I don’t enjoy small living spaces, but it’s worth it for me to live in a larger more expensive place.

3. How has this decision impacted your quality of life?

It’s only been a few months since I made the shift but so far, so good! I never realized how much of myself I was giving until I didn’t have any more to give.

Now, when I decide to do things, I base the decisions on my quality of life first and money second.

Here are two examples. I didn’t like my first job, so I interviewed with a few different companies. I had a handful of interviews, but only one place really stood out as somewhere I’d want to be. Unfortunately, they couldn’t afford to pay me my current rate, so I took a $5,000/year pay cut.

Old me would have stood firm on the pay and missed out on an excellent opportunity.

Now that I have a new job, I have a new commute. I decided to live closer to work, so I just moved into a new apartment.

I made the conscious decision that it would be better for my mental health to live in a nice place on my own, without roommates.

Because of this, I’ve doubled my housing expenses and pay 55% of my after-tax salary on it. Since I’m confident in my budgeting skills, I’m not as stressed about money as I otherwise might be.

So far, I’ve really enjoyed living here, and I’m very happy with my decision.

4. How did it impact your financial goals or timelines?

Timeline? What timeline?

When I first started working, my desire to achieve FIRE was ruled by what I didn’t like.

I didn’t like my job then, so I saved as much as possible to get away from the necessity of having a not so great job. My goal then was to retire by 35.

Along the way, as I ramped up the side hustles, my timeline got shorter until I experimented with entrepreneurship.

Now, I’m not entirely sure what I want from life.

I have a job I enjoy that provides definition and meaning to my life. I love living in HCOL DC.

Technically, I’m already Coast FI, which means that if I didn’t add any additional money to my investments, they would grow to the point that I could retire comfortably at traditional retirement age.

The great thing about being CoastFI at such a young age is getting to experiment with different living situations. When I got tired of living in a small Midwestern town, I quit my job and moved to a big Midwestern city to be self-employed. I enjoyed city life but not the entrepreneur lifestyle.

Now, I’m living in a huge East Coast metropolitan area with a new job and am now exploring what that life looks like.

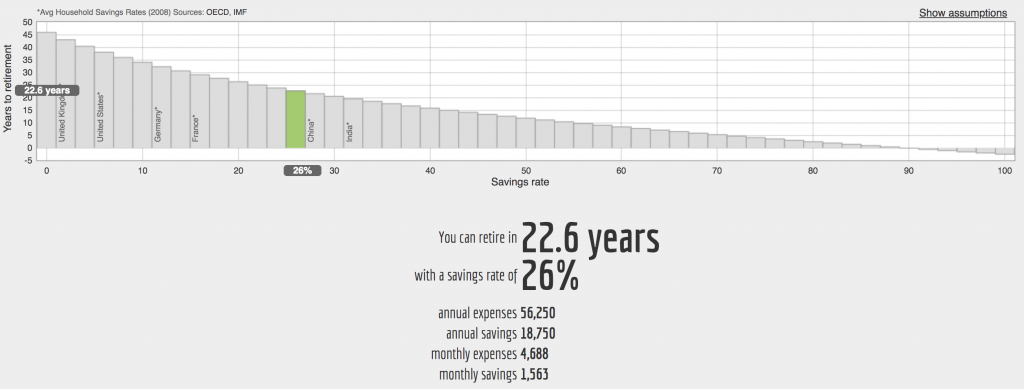

Since I’m still getting settled, my savings rate has fluctuated since moving here, but I think it’s going to settle down into the 20-30% range. This is a very respectable savings rate to have in such an expensive area.

Giving the savings I already have, my calculated retirement age is in 22 years at age 50. That is still very early by normal societal standards.

5. What enabled you to make this decision (i.e. what financial or social context helped)?

Honestly, the main reason I was able to make this decision was that I saved so aggressively early in my career. Because I found FIRE early, I made it my priority to save for retirement rather than spending on new cars or fancy vacations.

I got paid nearly double the average household income for my zip code. Having a high income allows you to optimize everything else more easily.

I lived in a low cost of living area. I kept my housing costs low by having roommates, living with others, and briefly house hacking my own property.

I wouldn’t be so far ahead if I had paid $1,895 a month for rent every year.

At the age of 28, I’ve saved over $200,000 towards retirement. I’m headed towards an early retirement at age 50 with a comfortable lifestyle. If I want to change anything, my timeline will only speed up from there.

6. Were there things in your life you adapted so you could continue to work toward your goals?

I got rid of things that didn’t make me happy.

I went over each activity in my life and asked myself, “Why am I doing this?”. If the answer wasn’t, “Because I want to/it makes me happy”, I got rid of it.

So many things in my life were the result of other’s expectations of me that I lost sight of what makes me, me.

I really liked the quote from Thor’s Mom to Thor in Avengers: Endgame (mild spoilers, maybe?).

“Everyone fails at who they’re supposed to be, Thor. The measure of a person, of a hero, is how well they succeed at being who they are.”

Frigga (Thor’s Mom) in Avengers: Endgame

I’ve failed at being the person I’m supposed to be. I am now damn sure I’m going to succeed at being me! After all, no one else can be me, so why was I trying to be someone else?

7. Why and when do you think someone might consider “downshifting?”

I think someone should consider downshifting before they hit a breaking point as I did.

If you find yourself starting to merely go through the motions every day or lose pleasure in activities that you once enjoyed, it’s probably worth sitting down and doing an evaluation on what makes you happy.

Then, only do those things! Life is too short to do things we don’t like!

8. How did your pursuit of FI help or hinder this decision?

Ha! This whole thing was because of FIRE!

Saving so aggressively early in my career has helped balance the less than optimal finance choices I’ve made lately. The actions I took at the beginning of my career made it so that I can make my current choices.

Of course, this is the opposite of a lot of stories I see online. Most people spend a lot early and then realize they need to save. I saved a lot early, and now I have the freedom to spend more.

9. What advice do you have for someone considering a similar decision?

Don’t delay! Only do things you want to do!

Know who you are and don’t let others pressure you into things. In this corner of the internet, people mean well and many will help you out in the long run.

Not everyone is meant to be an online entrepreneur. If it’s not for you and you try it, you’ll still be unhappy with your life. In the words of Sweet Brown, “Ain’t No One Got Time for That!”

Wow! What a fantastic interview with Gwen!

Sadly, it is not uncommon to see people in the personal finance community get to a point where the hustle and busyness cause too much stress and strain on our mental health. I’ve certainly been there.

What I love is that Gwen didn’t stay there and wait until she retired early to get a reprieve. She realized that financial freedom isn’t all or nothing.

Gwen hustled hard early in her career and achieved Coast FI, meaning that she wouldn’t need to add any additional money to her investment accounts and she could still retire comfortably at traditional retirement age.

Because super-early retirement is no longer her goal, she now gets to experiment with another new lifestyle design. Her decisions are now based on “quality of life first, money second.”

This goes to show that when you get to a level of financial stability, you can choose to ease up on your savings rate.

Some people do this by choosing to earn less. They work part-time jobs, lower-paying jobs they enjoy more or only work for a portion of the year.

Others choose to spend more to improve their quality of life. Some might choose to live in a high cost of living area or travel more frequently.

Gwen decided to do both. She decided to live in a high cost of living area without roommates, quit her side hustles, and take a lower-paying job. It definitely takes courage to do this, even when you have financial stability. Bravo, Gwen!

Like Gwen, we’ve chosen to use both levers to improve our lives. Earlier this year, I started working part-time. This decreased our income and dramatically improved our quality of life.

We have also chosen to live in a High Cost of Living area. We absolutely love living in Boston. Going against common wisdom, we’ve actually found that living in a HCOL area has fast-tracked our path to FI because of the availability of higher-paying jobs. I wonder if Gwen will also find this to be the case in DC.

I’m interested to see what additional lifestyle design experiments Gwen embarks on in the coming years.

If you’d also like to continue following Gwen’s journey, here’s where you can find her.

Blog: https://www.fierymillennials.com/

Twitter: @FieryMillennial

Instagram: @fierymillennials

Another great addition to the Slow FI series! Good interview, Gwen.

Similar to you, I’m coming to appreciate optimizing choices towards simplicity these days, rather than for the most financial gain. Having a clearer mind and fewer obligations is a wonderful form of wealth. It’s a reason why I won’t get into property investment, even if I’m leaving some money “on the table” – I just don’t want the stress and hassle, when basic index funds will get me there to FI in the end too.

“So many things in my life were the result of other’s expectations of me that I lost sight of what makes me, me.” I’m glad you’re finding yourself again! See you at FinCon.

What a great insight into Gwen’s story!

I agree. I’m so glad she was willing to share it with all of us!

Love the insight into Gwen’s slowFI journey. I knew she was pulling back on some of her projects, but I wasn’t exactly sure why, when she was making so much progress towards FI.

Now it makes so much sense. Congrats to her for reaching CoastFI at such a young age, which allows for mobility!

Exactly. I only followed on Twitter and read the misleading article, so I didn’t get the big picture. It’s great to see this story told as it’s much more helpful.

The problem with “hustle” is that it never really ends. I never want to be an “influencer” because it’s like you are always on the clock and/or being watched. Some people like that attention, but it’s too much work for me.

Hi,

Thanks for the comment. Yes, the article was completely misleading! I can also imagine that the full-time hustle would be hard. That is part of the reason why I’m planning to work until I feel like I could generate enough income only doing things I want to on the side. I’ll likely be working for a while longer before I’ll feel comfortable taking the leap, and I’m okay with that.

Thanks!

Jessica

Thanks for all of your support in my journey!

I spoke to Gwen at a movie premiere. She talked a little about the topics in this blog. I think its easy to get caught up in the fast path to FI if you listen to lots of Podcast and read lots of blogs. I think most folks in our community out there take the simple path to FI and manager it similar fashion. It would be interesting to understand how many are hustling and how many are taking the slow FI path in our community. I think it would be very lopsided!

Hey Accidental FI,

Thanks for the comment. Could you clarify whether you think the majority of the community is trying to take the fast or the slow path? I wasn’t quite sure from your comment. I’d be interested as well. I imagine that most are actually taking a slower path to FI, but people with those stories tend to be less well-known and thus we tend to not know about them. I could be wrong though.

I’d love to hear what you think!

Jessica

I think the blogger community is heavily weighted towards the hustle side but the vast majority of readers are on a slower path to FI.

This is a great point. I completely agree!

Great interview. Gwen, great job slowing down. It’s way better to find a moderate path that will work for you.

Hustling is better for after FI. You don’t have to stress about money and it’s just gravy. Unless you can hit the jackpot and make a ton of money from hustling, most people should stick with a good W2 job.

Good luck!

Thanks Joe! That hustle life isn’t for everyone for sure.

Looks like excellent choices for Gwen. Figure out the framework of life that works best and go with it. Ignoring labels or imposed ideas is a great freedom that she has found.

Thanks Pete! In some ways I have all the freedom in the world and in others, very little. It’s an interesting mix and one that I’m still exploring.

I that you no longer have a set end date. I think in some ways, not having one is a symptom of being happier with your life right now.